Exhibit 99.4

| | | |

Almacenes Éxito S.A.

Consolidated Financial Results 3Q25

Envigado, Colombia, November 13, 2025 – Almacenes Éxito S.A. (“Grupo Éxito” or “the Company”) (BVC: ÉXITO) announced its results for the third quarter ended September 30, 2025 (3Q25). All figures expressed in millions (M) and Billions (B) of Colombian pesos (COP) unless otherwise indicated and expressed on a short scale (COP B represent 1,000,000,000). Consolidated data includes results from Colombia, Uruguay and Argentina, and eliminations.

3Q25 Confirms Consistency in Strategy Driving Profitability and Efficiency

Key financial and operational highlights

Financial highlights

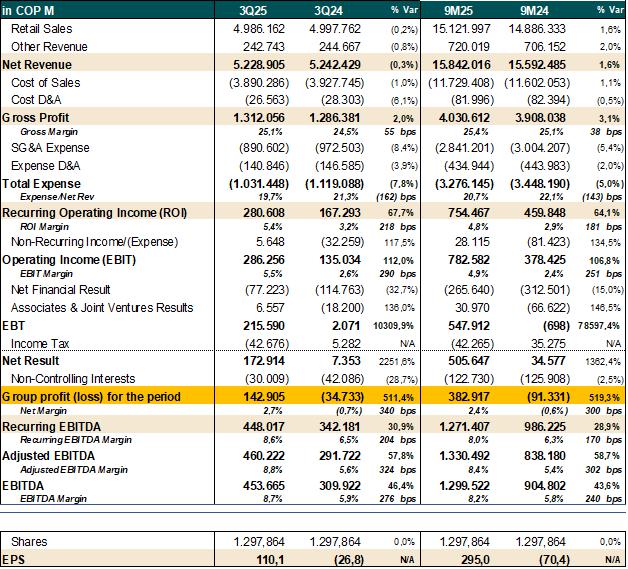

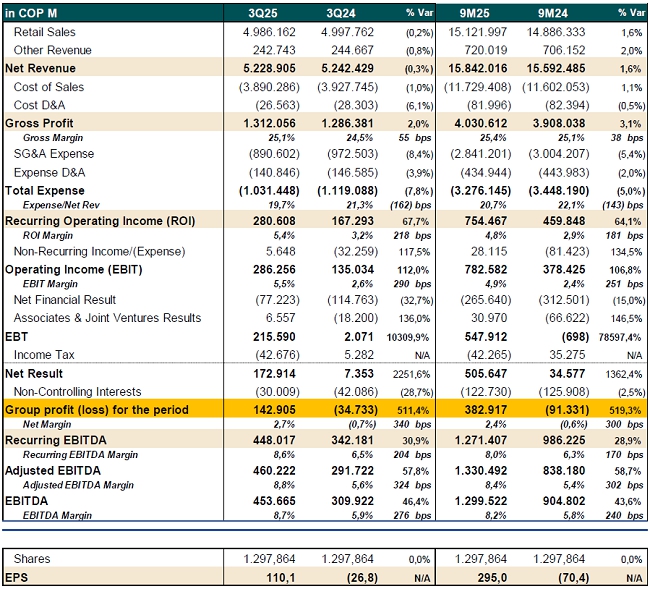

| ● | Consolidated net revenues recorded COP $5.2 billion during 3Q25, in line with 3Q24 and growing +3.9% excluding FX. Revenues from Colombia contributed 78.3% of the group’s consolidated total net revenue. The remaining income comes from Uruguay and Argentina. In the year to date, consolidated net revenues reached COP $15.8 billion, with a growth of +1.6% compared to the same period of the previous year, and +4.4% excluding FX. |

| ● | Gross profit reached COP $1.3 billion in 3Q25, with a margin that improved by +55 bps, reaching a level of 25.1% as a percentage of revenues. For the first nine months of the year, gross profit reached COP $4.0 billion, with a growth of 3.1% compared to the same period of the previous year. The results reflect the execution of commercial initiatives, driven by strategic pillars such as saving levers, brand unification and the increase in assortment. Additionally, other complementary businesses contributed to strengthening the Group’s ecosystem. |

| ● | Recurring EBITDA1 showed significant growth, driven by efficiencies in commercial margin, together with the rigorous execution of action plans in costs and expenses. This resulted in a 204 basis points improvement in the EBITDA margin, which stood at 8.6%, reaching COP $448 billion in 3Q25, representing a growth of 30.9% compared to the same period in 2024. In the year to date, recurring EBITDA reached COP $1.3 billion, with a growth of +28.9% vs the same period of the previous year. |

| ● | Positive net result of COP $143 billion during 3Q25 and COP $383 billion accumulated for the nine months of the year reflecting an improvement in operating performance, efficiencies in financial cost and debt levels, as well as the solid contribution of the complementary businesses. |

| ● | EPS2 of COP $110.1 per common share in the quarter (vs. COP -$26.8 reported in 3Q24). |

Operational highlights

| ● | LTM3 store expansion: 19 stores (Col 18 and Uru 1) for a total of 584 stores, 985 thousand square meters. The expansion strategy in Colombia focused on store conversions to the flagship brands of Éxito for the largest stores and Carulla for stores under 2,000 meters. |

| (1) | Recurring EBITDA refers to earnings before interest, taxes, depreciation and amortization excluding other non-recurring operating income (expense). (2) EPS considers the weighted average number of shares outstanding (IAS 33), corresponding to 1,297,864,359 shares. (3) Expansion from openings, reforms, conversions, and refurbishments. |

1

| | | |

Corporate Governance

| ● | July 16, 2025 - Approval of the cancellation of the BDR program |

| ● | August 4, 2025 – Approval of the cancellation of the Company’s registration as a category “A” foreign issuer in Brazil. |

| ● | August 13, 2025 – Quarterly Periodic Report |

| ● | September 16, 2025 - Grupo Éxito shares enter S&P Colombia Select index for the first time |

| I. | Consolidated Income Statement |

Note: Consolidated data includes results from Colombia, Uruguay and Argentina, eliminations and the currency effect of -4.0% in Net Revenues and +0.7% in Recurring EBITDA during 3Q25. In addition, the exchange effect of -2.7% on net income and -0.5% on recurring EBITDA during 9M25. Recurring EBITDA refers to earnings before interest, taxes, depreciation and amortization adjusted by other non-recurring operating income (expenses). Adjusted EBITDA refers to earnings before interest, taxes, depreciation and amortization plus the results of associates and joint ventures. EPS considers the weighted average number of shares outstanding (IAS 33), corresponding to 1,297,864,359 shares.

2

| | | |

| II. | Net Revenue Performance |

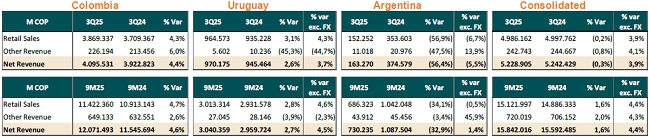

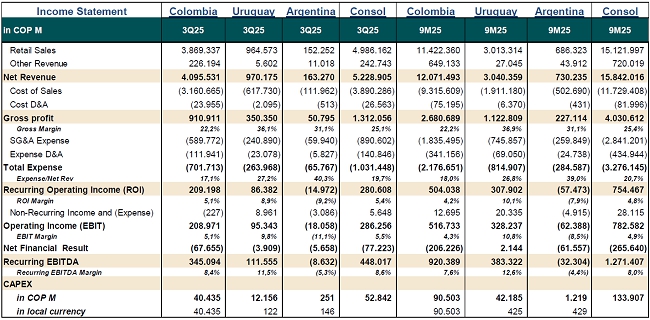

| ● | Consolidated net revenues grew +3.9% excluding FX (-0.3% in COP), reaching COP $5.2 billion during 3Q25. 78.3% of consolidated net revenues came from Colombia, highlighting the performance of the non-food category (+9.1% vs 3Q24). Operations in Uruguay and Argentina contributed with the remaining 21.7%. For 9M25, consolidated net revenues totaled COP $15.8 billion, with a growth of +4.4% excluding FX (+1.6% in COP), compared to the same period of the previous year. |

Consolidated retail sales reached COP $5.0 billion in 3Q25, reflecting a growth of +3.9% excluding FX (-0.2% in COP). In the year to date, consolidated net sales totaled COP $15.1 billion. During the third quarter of 2025, same- store sales (SSS) grew +5.4%, excluding FX. The overall sales performance is attributable to: (i) the result of the successful commercial strategies implemented in Colombia, which allowed sales growth of +4.3% for the third quarter of 2025, (ii) a consistent growth in sales in Uruguay of +4.3% during 3Q25, excluding FX, (iii) the contribution of the expansion with 19 stores LTM1 (Col 18 and Uru 1) and (iv) the dificult sales performance in Argentina impacted by lower consumption, currency devaluation and the optimization of the store portfolio.

Other consolidated revenues increased by +4.1% in 3Q25, excluding FX (-0.8% in COP), driven by the contribution of the real estate business in Colombia and Argentina.

Colombia: During the third quarter of 2025, the economic environment in Colombia continued to be challenging, although with signs of stabilization. By September 2025, year-on-year inflation stood at 5.2%, while food inflation was 6.1%, compared to 2.3% in the same period of the previous year. On the other hand, internal food inflation was 0.89 p.p. lower than national food inflation. Despite the challenges, consumer confidence recovered, with households prioritizing essential spending. The confidence index reached its highest level in two years, with a record of 1.6 p.p. in September 2025 (-16 p.p. in the same period of 2024). In response to inflation, the central bank kept the interest rate at 9.25% for 3Q25, with a moderate monetary stance.

3

| | | |

During the third quarter of 2025, the operation in Colombia contributed 78.3% to the group’s consolidated revenues, posting a growth of +4.4% and reaching COP $4.1 billion, confirming the positive trend recorded during 2025. During the first nine months of the year, net income totaled COP $12.1 billion with a growth of +4.6%, compared to the same period of the previous year.

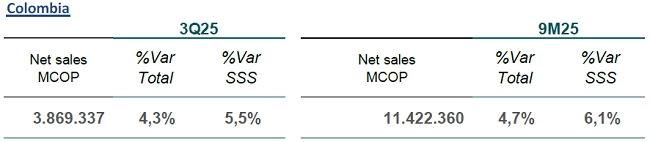

Net sales totaled COP $3.9 billion (+4.3%) and SSS (+5.5%), mainly explained by the recovery of the non-food category (+9.1%), driven by double-digit growth in electro-digital (+13.1%). On the other hand, food sales grew +2.5%, with the fresh category standing out with a growth of +5.4%. In addition, omnichannel sales continue to strengthen with a share of 14.6% (+30 bps vs 3Q24), in addition to the contribution of 18 stores opened, converted and refurbished in the last 12 months. Net sales for Colombia during the first nine months of 2025 grew by +4.7% reaching COP $11.4 billion and SSS grew +6.1%.

Éxito brand stores accounted for 70% of sales in Colombia, followed by Carulla stores that accounted for 19% and the low-cost & others1 which includes Super Inter, Surtimax and Surtimayorista banners, allies, institutional sales, third-party sellers, the sale of property development projects (inventory) and other, accounted for 11% of sales in 3Q25.

Note: SSS in local currency, includes the effect of conversions and excludes the calendar effect of -1.17% in 3Q25 and -0.62% in 9M25. (1) The segment includes Retail Sales from Surtimax, Super Inter and Surtimayorista brands, allies, institutional and third-party sellers, and the sale of property development projects (inventory) of COP $2.8 B during 9M24 vs COP $3.8 B during 9M25.

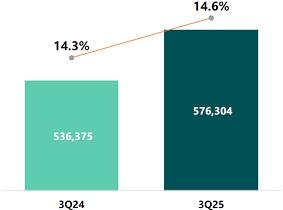

Omni-channel sales in Colombia (including websites, marketplace, home delivery, Shop&Go, Click&Collect, digital catalogs and virtual B2B and Midescuento), grew +7.4% vs 3Q24, reaching COP $576 billion, for 9M25 omnichannel sales reached COP $1.6 B, growing 6%. In the third quarter, omnichannel sales share reached 14.6% (vs 14.3% in 3Q24 in comparable terms excluding ISOC channel), driven by the growth of the non-food category of +12.1% (16.8% share of non-food sales) and added to the performance of the food category that grew +5.2% (13.8% share of food sales).

4

| | | |

Omni-channel sales and share on sales

Note: data in COP M

The main KPIs during 3Q25 compared to the same period last year in comparable terms excluding the ISOC channel from the base, were as follows:

| o | Orders: reached 6.8 million (+14.8%) during 3Q25. |

| o | E-commerce sales: reached COP $ 224.7 B during 3Q25 (+11.8%). |

| o | MiSurtii sales: reached COP $18.7 B and 23,000 orders. |

| o | Apps: Sales totaled COP $53.1 B (+15.1%) and reached 173,614 orders during 3Q25. |

| o | Rappi’s deliveries grew 18.6% during 3Q25. |

| o | Marketplace revenues: reached COP $47 B during 3Q25 and added more than 1,427 sellers. |

| o | Turbo: orders grew 26.6% during 3Q25 through Rappi (a leading last-mile delivery platform in Latin America). |

| ● | Other revenues increased 6.0% during 3Q25, explained by the contribution of complementary businesses, mainly due to recurring revenues from the Real Estate business (+11% vs 3Q24) and the contributions from the mobile and travel businesses. |

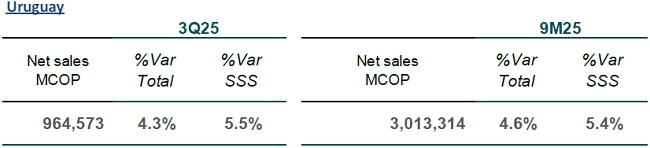

Uruguay: Uruguay contributed with 19.3% of consolidated net sales during 3Q25. Inflation for the last 12 months to September was 4.25% (compared to 5.32% in September 2024) and the food component registered 4.65% over the last 12 months.

Net sales and SSS grew +4.3% and +5.5% respectively excluding FX, driven by the contribution of the 32 Fresh Market stores (+6.1% growth vs 3Q24) in a stable political and economic environment. During the first nine months of 2025, net sales reached COP $3.0 B with a growth of 4.6% and SSS 5.4% excluding FX when compared to the same period of the previous year.

The operation in Uruguay maintained a stable market share at 42.2% (-0.3% vs 9M24) in terms of SSS as of September, according to Scanntech, driven by: (i) the strong sales performance of all brands and (ii) the contribution of the 32 Fresh Market stores.

5

| | | |

Note: SSS without the currency effect, includes the effect of conversions and the calendar effect of 0.01% and 0.16% during 3Q25 and 9M25 respectively.

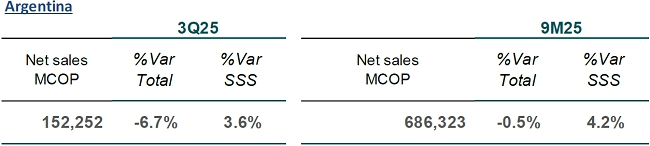

Argentina: The operation in Argentina contributed with 3.1% of consolidated net sales and results in Colombian pesos included a -53.9% exchange effect on net revenues during 3Q25.

Net revenues in Argentina for 3Q25 reached to COP $163.2 B (-5.5% excluding FX) and 9M25 COP $730.2 B (+1.4% excluding FX). Net sales were COP $152.2 B (-6.7% excluding FX and +3.6% in SSS) during 3Q25. Inflation in the last 12 months to September was 31.8% according to INDEC, which compares to a 209% reported during the same period of the previous year. Net sales were affected by lagging consumption and store closures.

During 3Q25, the real estate business showed strong performance (+13.9% growth excluding FX) thanks to improved commercial trends and healthy occupancy levels.

Note: SSS without the currency effect, includes the effect of conversions and the calendar effect of -0.07% and -0.3% during 3Q25 and 9M25 respectively.

6

| | | |

| III. | Operating Performance |

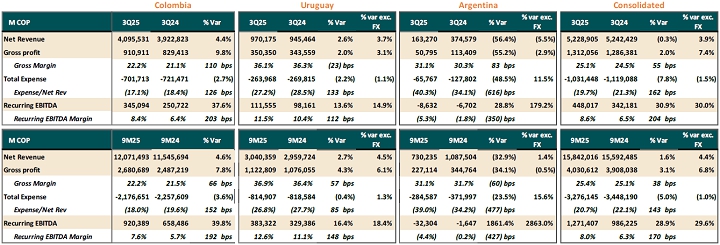

Note: The scope of Colombia includes Almacenes Éxito S.A. and its subsidiaries. The consolidated data in COP include the currency effect of -4.0% on revenues and 0.7% on recurring EBITDA in 3Q25, -2.7% and -0.5 respectively for 9M25. Recurring EBITDA refers to earnings before interest, taxes, depreciation and amortization adjusted by other non-recurring operating income (expenses).

Consolidated Gross Profit increased +7.4% excluding FX (+2.0% in COP) during 3Q25, and the margin reached 25.1% (+55 bp) as a percentage of revenues. Improvement in margins in Colombia and Argentina thanks to advances in commercial strategy, cost reduction and control of shrinkage levels, which offset the slight deterioration of margins in Uruguay.

| ● | Gross profit in Colombia grew +9.8% to a margin of 22.2% (+110 bps) as a percentage of revenues during 3Q25. The improvement reflects the contribution of all businesses, as well as efficiencies in logistics costs and shrinkage levels. Gross profit grew by +7.8% with a margin of 22.2% (+66 bps) as a percentage of revenues during 9M25. |

| ● | Gross profit in Uruguay increased +3.1% excluding FX (+2.0% in COP) during 3Q25 and the margin as a percentage of revenues was 36.1% (-23 bps) with cost pressures that were partially mitigated by efforts on reducing shrinkage levels. During 9M25, gross profit grew by +6.1% excluding FX to a margin of 36.9% (+57 bps vs. the same period last year). |

| ● | Gross profit in Argentina decreased by -2.9% during 3Q25 excluding FX, however it reached a margin of 31.1% (+83 bps) as a percentage of revenues, thanks to a strict cost control. Gross profit decreased -0.5% excluding FX during 9M25, reaching a margin of 31.1% (-60 bps vs 3Q24) as a percentage of revenues. |

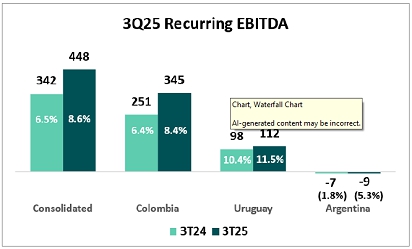

Consolidated Recurring EBITDA reached COP $448 billion during 3Q25 and COP $1.3 B in 9M25, with double-digit growth of +30.9% and +28.9% respectively compared to the same periods of the previous year. Expenses efficiencies across the region explains a decrease of -1.5% excluding FX and an improvement in its margin as a percentage of net revenues (+109 bps) which, added to a better performance in gross profit, contributed to an improvement of +204 bps in the recurring EBITDA margin1 reaching 8.6% as a percentage of revenues in 3Q25 and 8.0% (+170 bps) in 9M25.

7

| | | |

Note: COP Data Billions (1) Recurring EBITDA refers to earnings before interest, taxes, depreciation and amortization adjusted by other non-recurring operating income (expense)

Colombia: Recurring EBITDA grew by +37.6% during 3Q25 and the margin was 8.4% (+203 bps). For the first nine months of the year recurring EBITDA grew 39.8% with a margin of 7.6% as a percentage of revenues. Expenses decreased for both the quarter and the year to date with -2.7% and -3.6% respectively, despite inflationary pressures and thanks to cost and expenses efficiency plans.

Uruguay: Recurring EBITDA grew by +14.9% excluding FX (+13.6% in COP) during 3Q25 compared to the same period last year, reaching a margin of 11.5% (+112 bps) as percentage of net income, reflecting consistent sales growth and efficiencies in selling, general and administrative expenses (+133 bps). The cumulative figure for the year presented a recurring EBITDA growing by +16.4% with a margin of 12.6% (148 bps). The operation in Uruguay continued as the group’s most profitable business unit.

Argentina: Recurring EBITDA reached a margin of –5.3% (-350 bps) as a percentage of net revenues in 3Q25 and for the year-to-date recurring EBITDA reflected a margin of -4.4% (427 bps). Corrective measures being implemented to drive a change in trend.

8

| | | |

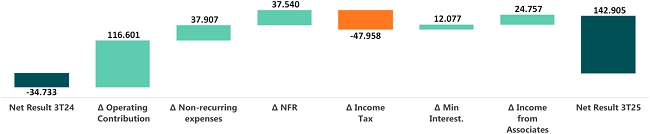

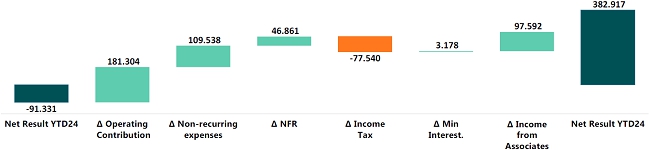

| IV. | Group Net Result |

Grupo Éxito achieved a net result of $143 billion Colombian pesos for the third quarter and $383 billion in the first nine months of the year, in contrast to negative results in the same periods of the previous year. The performance is explained by: (i) the operating result in Colombia and Uruguay, which fully compensate the low performance in Argentina; (ii) lower non-recurring expenses from the restructuring process and closure of unprofitable stores in the base; (iii) lower financial costs; and (iv) contribution of complementary businesses, mainly Tuya and Puntos Colombia. In addition, it includes a non-recurring positive effect derived from the recognition of a greater stake of the Group in the Uruguay operation, allowing it to achieve a net margin of 2.7% and an improvement of 340 basis points compared to the third quarter of 2024.

Note: data in M COP. Consolidated data include results from Colombia, Uruguay and Argentina, eliminations and the currency effect (-4.0% in revenues and +0.7% in recurring EBITDA in 3Q25, -2.7% and -0.5% in 9M25 respectively).

Earnings Per Share (EPS)

| ● | Diluted EPS was COP $110.1 per common share in 3Q25 compared to COP $-26.8 reported in the same period of the previous year. |

9

| | | |

| V. | CapEx and expansion |

CapEx

| ● | Consolidated CapEX during 3Q25 reached COP$ 52.8 billion, of which 62% was allocated to expansion, innovation, omnichannel and digital transformation activities during the period, while the remaining went to maintaining and supporting operational structures, upgrading IT systems and logistics. |

Retail expansion

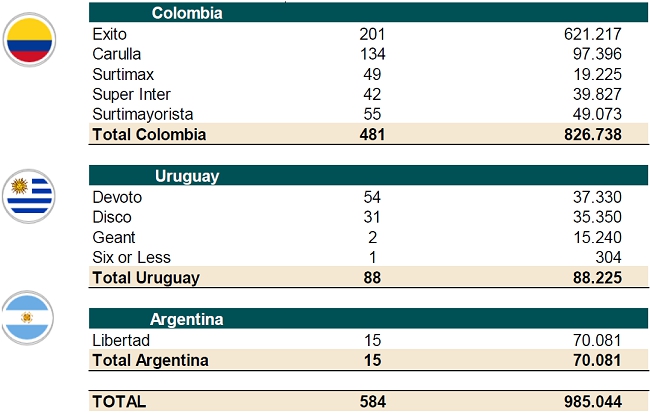

| ● | In the last 12 months of the year, Grupo Éxito added 19 stores for openings, renovations, conversions and remodeling (18 in Colombia and 1 in Uruguay). The Company totaled 584 retail stores, geographically diversified as follows: 481 stores in Colombia, 88 in Uruguay and 15 in Argentina, and the consolidated sales area reached 985 thousand square meters. The store count did not include the 1,900 allies (+90 last 12 months) in Colombia. |

| ● | In line with the company’s strategy, aiming at efficiencies to increase profitability, during the third quarter of 2025, 2 underperforming stores were closed in Colombia, 1 in Uruguay and 5 in Argentina. |

10

| | | |

| VI. | Cash and debt at the holding level |

Net financial debt:

| ● | Net debt-to-EBITDA ratio remained stable in 0.9X, reflecting operational strength and consistent cash flow generation. |

| ● | Efficiencies in financial expenses due to renegotiation and reduction of interest rates added to the decrease in the reference rate. |

11

| | | |

| VII. | Conclusion |

Grupo Éxito showed a positive evolution across its key indicators, with progress in operational efficiency, strengthening our ecosystem, and solid financial management. Although challenges remain in Argentina, the Group has confirmed the ability to adapt and execute, consolidating its position as a regional leader, focused on sustainable growth and long-term value creation.

12

| | | |

| VIII. | Conference Call and Webcast |

Almacenes Éxito S.A.

(BVC: ÉXITO)

Cordially invites you to participate in its

Third Quarter 2025 Results Conference Call

Date: Thursday, November 13, 2025

Time: 9:00 a.m. Eastern Time

9:00 a.m. Colombia Time

Presenting for Grupo Exito:

Juan Carlos Calleja Hakker, Chief Executive Officer

Fernando Carbajal, Chief Financial Officer | IRO

Laura Botero, Investor Relations Director

To register and get notified via email, please click here:

Register

To directly participate, please click here:

Join Microsoft Teams Meeting

Almacenes Éxito S.A. will report its third Quarter 2025 Earnings

on Wednesday, November 12, 2025.

3Q25 results will be accompanied by a presentation that will be available on the company’s website at www.grupoexito.com.co under “Shareholders and Investors” on the following link: https://www.grupoexito.com.co/en/financial-information

For more information please contact:

Almacenes Éxito S.A. Investor Relations

exitoinvestor.relations@grupo-exito.com

https://www.grupoexito.com.co/en/contact-shareholders-investors

13

| | | |

Appendices

Notes:

| ● | Numbers expressed in short scale, COP billion represent 1,000,000,000. |

| ● | Growth and variations expressed in comparison to the same period last year, except when stated otherwise. |

| ● | Sums and percentages may reflect discrepancies due to rounding of figures. |

| ● | All margins calculated as percentage of Net Revenue. |

| ● | Percentages represent relative proportions, and as such they cannot be directly added or subtracted from each other because they are not absolute numeric values. |

Glossary:

| ● | Colombia results: consolidation of Almacenes Éxito S.A. and its subsidiaries in the country. |

| ● | Consolidated results: Almacenes Éxito results, Colombian and international subsidiaries in Uruguay and Argentina. |

| ● | Adjusted EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization plus Associates & Joint Ventures results. |

| ● | EPS: Earnings Per Share calculated on an entirely diluted basis. |

| ● | Financial Result: impacts of interests, derivatives, financial assets/liabilities valuation, FX changes and other related to cash, debt, and other financial assets/liabilities. |

| ● | Free cash flow (FCF) = Net cash flows used in operating activities plus Net cash flows used in investing activities plus Variation of collections on behalf of third parties plus Lease liabilities paid plus Interest on lease liabilities paid (using variations for the last 12 M for each line) |

| ● | CAGR: Compound Annual Growth Rate |

| ● | GLA: Gross Leasable Area. |

| ● | GMV: Gross Merchandise Value. |

| ● | Holding: Almacenes Éxito results without Colombian and international subsidiaries. |

| ● | Net Revenue: Total Revenue related to Retail Sales and Other Revenue. |

| ● | Retail Sales: sales related to the retail business. |

| ● | Other Revenue: revenue related to complementary businesses (real estate, insurance, travel, etc.) and other revenue. |

| ● | Recurring EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization Operating Profit adjusted by other non-recurring operational income (expense). |

| ● | Recurring Operating Profit (ROI): Gross Profit adjusted by SG&A expense and D&A. |

| ● | SSS: same-store-sales levels, including the effect of store conversions and excluding the calendar effect. |

14

| | | |

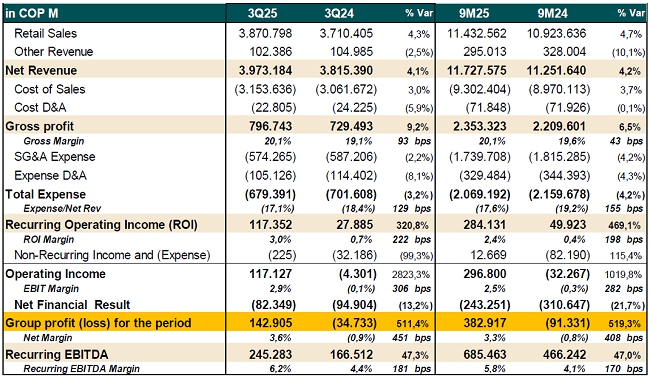

| 1. | Consolidated Income Statement |

Note: Consolidated data includes results from Colombia, Uruguay, and Argentina, eliminations, and the FX effect of -4.0% on consolidated net revenue and 0.7% on Recurring EBITDA during Q3 2025. Additionally, a FX exchange effect of -2.7% on Net Revenue and -0.5% on Recurring EBITDA was recorded during 9M25. Recurring EBITDA refers to earnings before interest, taxes, depreciation, and amortization, adjusted by other non-recurring operating income (expenses). Adjusted EBITDA refers to earnings before interest, taxes, depreciation, and amortization plus the results of associated and joint ventures. EPS is based on the weighted average number of shares outstanding (IAS 33), totaling 1,297,864 shares.

15

| | | |

| 2. | Income Statement and CAPEX by Country |

Notes: Consolidated data includes results from Colombia, Uruguay, and Argentina, eliminations, and the FX effect of -4.0% on Net Revenue and 0.7% on Recurring EBITDA during Q3 2025, and -2.7% and -0.5%, respectively, during 9M25. Recurring EBITDA refers to earnings before interest, taxes, depreciation, and amortization, adjusted by other non-recurring operating income (expenses). The scope for Colombia includes the consolidation of Almacenes Éxito S.A. and its subsidiaries in the country. Data reported in COP includes a FX effect of -1.1% in Uruguay on Net Revenue and Recurring EBITDA during Q3 2025, and -53.9% in Argentina, respectively, for 9M25: -1.7% for Uruguay and -33.8% for Argentina, calculated using the average and closing exchange rates.

16

| | | |

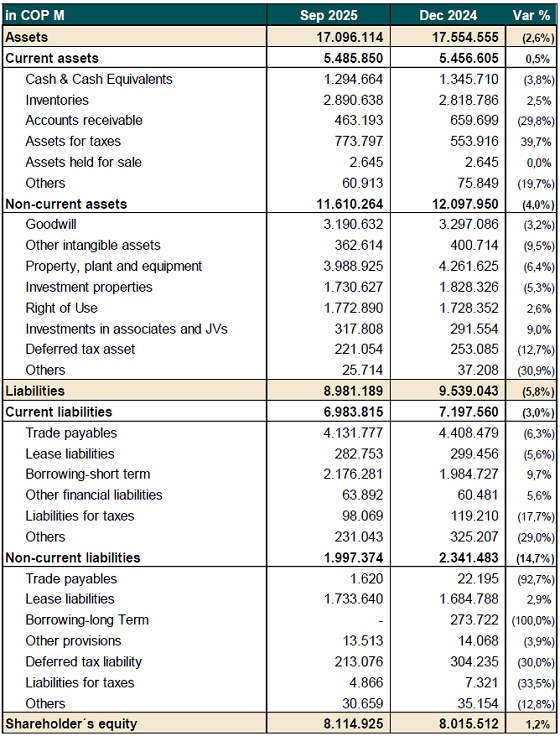

| 3. | Consolidated Balance Sheet |

Note: Consolidated figures include data from Colombia, Uruguay, and Argentina.

17

| | | |

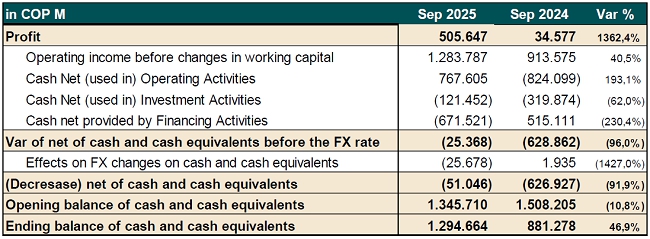

| 4. | Consolidated Cash Flow |

Note: Consolidated figures include data from Colombia, Uruguay, and Argentina.

| 5. | Almacenes Éxito1 Income Statement |

| (1) | Holding: Almacenes Éxito – Results excluding subsidiaries in Colombia. Recurring EBITDA refers to earnings before interest, taxes, depreciation, and amortization, adjusted by other non-recurring operating income (expenses). |

18

| | | |

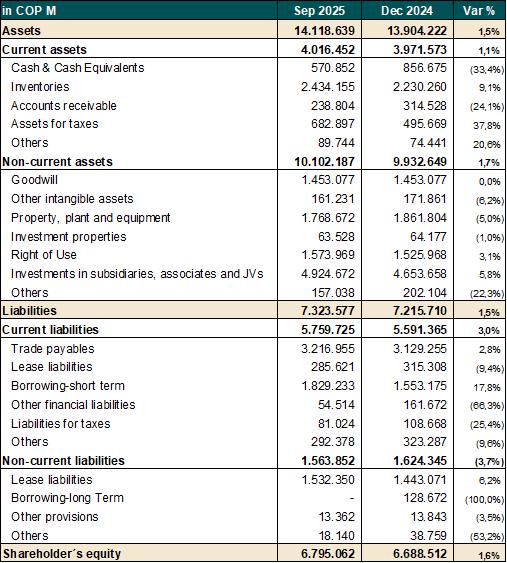

| 6. | Almacenes Éxito1 Balance Sheet |

| (1) | Holding: Almacenes Éxito Results without Colombia subsidiaries. |

19

| | | |

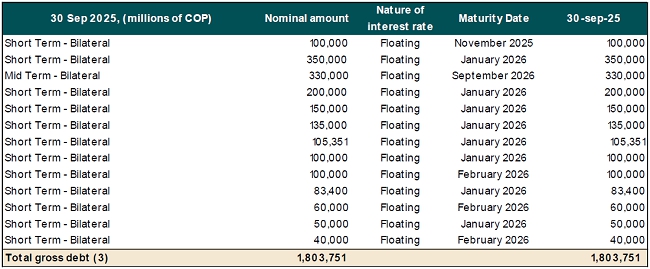

| 7. | Debt by country, currency, and maturity |

| (1) | Debt without contingent warranties and letters of credit |

| (2) | Other Collections included and positive hedging valuation not included |

Holding Gross debt by maturity

| (3) | Debt at the nominal amount |

Note: The Colombia perimeter includes the consolidation of Almacenes Éxito S.A. and its subsidiaries in the country. 1) Debt without contingent warranties and letters of credits. (2) Holding gross debt issued 100% in Colombian Pesos with an interest rate below IBR3M + 2.0%, debt at the nominal amount. IBR 3M (Indicador Bancario de Referencia) – Market Reference Rate: 9.25%; other collections included, and positive hedging valuation not included. (3) Debt at the nominal amount.

20

| | | |

| 8. | Stores and Selling Area |

Note: The store count does not include the 1,900 allies in Colombia.

21

| | | |

Note on Forward-Looking Statements

| ● | This document contains certain forward-looking statements based on data, assumptions, and estimates, that the Company believes are reasonable; however, it is not historical data and should not be interpreted as guarantees of its future occurrence. The words “anticipates”, “believes”, “estimates”, “expects”, “plans” and similar expressions, as they relate to the Company, are intended to identify forward-looking statements. Statements regarding the declaration or payment of dividends, the implementation of principal operating and financing strategies and capital expenditure plans, the direction of future operations and the factors or trends affecting financial condition, liquidity or results of operations, expectations in connection with the company’s ESG plans, initiatives, projections, goals, commitments, expectations or prospects, including ESG-related targets and goals, are examples of forward-looking statements. Although the Company’s management believes that the expectations and assumptions on which such forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements. |

| ● | Grupo Éxito operates in a competitive and rapidly changing environment; therefore, it is not able to predict all the risks, uncertainties or other factors that may affect its business, their potential impact on its business, or the extent to which the occurrence of a risk or a combination of risks could have results that are significantly different from those included in any forward-looking statement. Important factors that could cause actual results to differ materially from those indicated by such forward-looking statements, or that could contribute to such differences, include, without limitation, the risks and uncertainties set forth under the section “Item 3. Key Information – D. Risk Factors” in the Company’s registration statement on Form 20-F filed with the Securities and Exchange Commission on April 30, 2025. |

| ● | The forward-looking statements contained in this document are made only as of the date hereof. Except as required by any applicable law, rules or regulations, Grupo Éxito expressly disclaims any obligation or undertaking to publicly release any updates of any forward-looking statements contained in this press release to reflect any change in its expectations or any change in events, conditions, or circumstances on which any forward-looking statement contained in this document is based. |

| ● | Reconciliations of the non-IFRS financial measures in this webcast are included at the appendices to this webcast presentation. |

| ● | Figures expressed in Colombian pesos in this presentation follow the short-scale convention. Accordingly, billions refer to thousands of millions and trillions refer to millions of millions. |

22

| | | |

IR and PR contacts

Laura Botero M.

Investor Relations Director.

+57 (604) 6049696 Ext 306560

ainvestor@grupo-exito.com

Cra 48 No 32 B Sur 139, Envigado, Colombia

Claudia Moreno B.

PR and Communications Director

+(57) 604 96 96 ext. 305174

claudia.moreno@grupo-exito.com

Cr 48 No. 32B Sur – 139 – Envigado, Colombia

Company Description

Grupo Éxito is the leading food retail platform in Colombia and in Uruguay and has a relevant presence in the north-east of Argentina. The Company´s great capacity to innovate, has allowed it to transform and adapt quickly to new consumer trends and increased its competitive advantages supported by the quality of its human talent.

Grupo Éxito leads omni-channel in the region and has developed a comprehensive ecosystem focused on the omni-client, to whom it offers the strength of its brands, multiple formats and a wide range of channels and services to facilitate their shopping experience.

The diversification of its retail revenue through traffic and asset monetization strategies, has allowed Grupo Éxito to be a pioneer in offering a profitable portfolio of complementary businesses, such as, its real estate with shopping centers in Colombia and Argentina and financial services such as credit card, virtual wallet, and payment networking. The Company also offer other businesses in Colombia, such as travel, insurance, mobile and money transfers.

In 2019, Grupo Éxito officially launched its Digital Transformation strategy and has consolidated a powerful platform with well-recognized websites exito.com and carulla.com in Colombia, devoto.com and geant.com in Uruguay, and hiperlibertad.com in Argentina. Moreover, the Company offers click and collect services, digital catalogues, home delivery and growing channels such as Apps and Marketplace, through which Grupo Éxito has achieved an impressive digital coverage in the countries where it operates.

In 2024, consolidated Net Revenue reached COP $21.9 billion driven by strong retail execution, successful omni-channel strategy in the region and innovation in retail models, as well as the implementation of the three major initiatives for the development of its Colombian operation: brand unification, assortment expansion and savings levers. The Company operated 623 stores through multi-formats and multi-brands: hypermarkets under Éxito, Geant and Libertad brands; premium supermarkets with Carulla, Disco and Devoto; proximity under Carulla and Éxito, Devoto and Libertad Express brands. In low-cost formats, the Company operates banners Surtimax, Super Inter and Surtimayorista in Colombia and Mini Mayorista in Argentina.

23