Exhibit 99.6

2024 Annual Report

Exhibit 99.6

2024 Annual Report

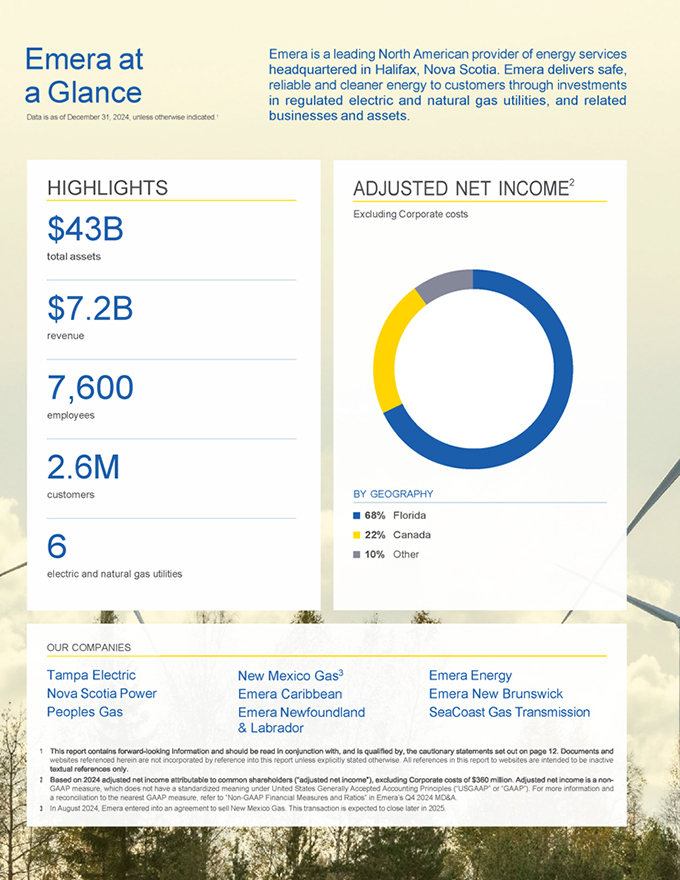

Emera at a Glance Data is as of December 31, 2024, unless otherwise indicated.1 Emera is a leading North American provider of energy services headquartered in Halifax, Nova Scotia. Emera delivers safe, reliable and cleaner energy to customers through investments in regulated electric and natural gas utilities, and related businesses and assets. HIGHLIGHTS $43B total assets $7.2B revenue 7,600 employees 2.6M customers 6 electric and natural gas utilities ADJUSTED NET INCOME2 Excluding Corporate costs BY GEOGRAPHY 68% Florida 22% Canada 10% Other OUR COMPANIES Tampa Electric New Mexico Gas3 Emera Energy Nova Scotia Power Emera Caribbean Emera New Brunswick Peoples Gas Emera Newfoundland SeaCoast Gas Transmission & Labrador 1 this report contains forward-looking information and should be read in conjunction with, and is qualified by, the cautionary statement set out on page 12 documents and websites referenced herein are not incorporated by reference into this report unless explicitly stated otherwise. All references in this report to websites are intended to be inactive textual references only. 2 Based on 2024 adjusted net income attributable to common shareholders (“adjusted net income”), excluding corporate costs of $360 million, adjusted net income is a non- GAAP measure, which does not have a standardized meaning under United States Generally Accepted Accounting Principles (“USGAAP” or “GAAP”). For more information and a reconciliation to the nearest GAAP measure, refer to “Non-GAAP Financial Measures and Ratios” in Emera’s Q4 2024 MD&A. 3 In August 2024, Emera entered into an agreement to sell New Mexico Gas. This transaction is expected to close later in 2025.

Why Invest in Emera Emera is at the forefront of a transformative era in energy with robust opportunities to invest on behalf of customers across the portfolio. Our proven strategy and operational excellence ensure we can capitalize on these opportunities and deliver earnings, cash flow and dividend growth for investors. PREMIUM PORTFOLIO OF REGULATED VISIBLE GROWTH PLAN UTILITIES FOCUSED IN FLORIDA ~70% $20B capital investment plan through 2029, focused on grid of adjusted net income,1 excluding Corporate costs, reliability, resiliency & modernization, system expansion to comes from our Florida operations meet customer growth, renewable integration, technology and customer facing solutions ~80% 7% to 8% of capital plan through 2029 is being invested in Florida, annualized, forecasted rate-base growth through 2029 supporting strong customer growth at Tampa Electric and Peoples Gas CONSTRUCTIVE REGULATORY ENVIRONMENTS RELIABLE EARNINGS AND DIVIDEND GROWTH Highly rated 18 years regulatory environments of consecutive dividend growth 1-2% 98% annual dividend growth target of adjusted net income,1 excluding Corporate costs, derived from our regulated utilities 5-7% average adjusted EPS2 growth target through 20273 1 Based on 2024 adjusted net income, excluding Corporate costs of $360 million. Adjusted net income is a non-GAAP measure which does not have standardized meaning under USGAAP. For more information and reconciliation to the nearest GAAP measure, refer to “Non-GAAP Financial Measures and Ratios” in Emera’s Q4 2024 MD&A. 2 Adjusted earnings per share (“EPS”) is a non-GAAP ratio, which does not have standardized meaning under USGAAP. For more information, refer to “Non-GAAP Financial Measures and Ratios” in Emera’s Q4 2024 MD&A. 3 Adjusted EPS growth forecast uses 2024 as base year.

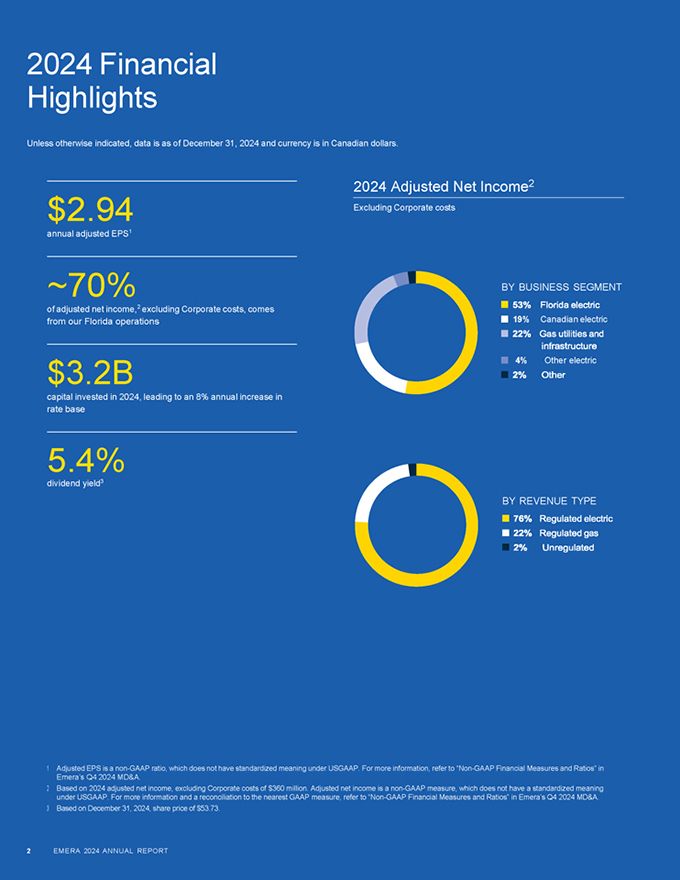

EMERA 2024 ANNUAL REPORT 1 2024 Financial Highlights Unless otherwise indicated, data is as of December 31, 2024 and currency is in Canadian dollars. $2.94 annual adjusted EPS1 ~70% of adjusted net income,2 excluding Corporate costs, comes from our Florida operations $3.2B capital invested in 2024, leading to an 8% annual increase in rate base 5.4% dividend yield3 2024 Adjusted Net Income2 Excluding Corporate costs 1 Adjusted EPS is a non-GAAP ratio, which does not have standardized meaning under USGAAP. For more information, refer to “Non-GAAP Financial Measures and Ratios” in Emera’s Q4 2024 MD&A. 2 Based on 2024 adjusted net income, excluding Corporate costs of $360 million. Adjusted net income is a non-GAAP measure, which does not have a standardized meaning under USGAAP. For more information and a reconciliation to the nearest GAAP measure, refer to “Non-GAAP Financial Measures and Ratios” in Emera’s Q4 2024 MD&A. 3 Based on December 31, 2024, share price of $53.73. 2 EMERA 2024 ANNUAL REPORT

OUR STRATEGY We seek reliable, growing, forward-thinking utility investment opportunities, focused on premium operations in high-growth jurisdictions, a robust capital investment strategy, and a thoughtful approach to risk management, all of which drive value and steady growth for our shareholders. OUR PURPOSE Energizing modern life and delivering a cleaner energy future for all. OUR VISION To be the energy provider of choice for our customers, the employer of choice for our people and a preferred choice for investors. OUR VALUES Our core values shape our culture and guide our work every day. We put safety above all else. We put customers at the centre of everything we do. We value candour, respect and collaboration. We care for each other, the environment and our communities. We set a high bar and take on big things. CLIMATE PROGRESS Building on more than two decades of cost-effective investment, we’re proud of our track record with system enhancements and reductions in CO2 emissions that have addressed government requirements along a path to net zero by 2050.1 1 Achieving our vision on this timeline is subject to external factors beyond our control and dependent upon decisions of, and/or support from, others including government, regulators, independent system operators, independent power producers, interconnected utilities, partners, investors, customers and Indigenous communities. It is also reliant on the development and/or commercialization of new and emerging technologies and/or the use of offsets. Shifts in government and regulatory policies/programs may impact our projects and progress. We will only proceed with forward-looking investments where we can demonstrate to the satisfaction of regulators that such investments are prudent and the most cost-effective solution for customers within the applicable legislative and regulatory regimes. 2 Includes provincial procurement programs and independent power purchase agreements. 3 Our reductions in CO2 emissions, coal used in generation (GWh), and our net-zero vision are compared to 2005 levels and include CO2 Scope 1 generation emissions for Tampa Electric and Nova Scotia Power only. These values are still undergoing review and verification. We have previously shared an internal 2025 target to achieve a 55% reduction in CO2 emissions compared to 2005 levels. 4 90% of our 2025-2029 capital plan is focused on cost-effective investments in grid reliability and modernization, renewable integration and technological innovation. 5. Where required by legislation or otherwise proven to be cost effective for customers. EMERA 2024 ANNUAL REPORT 3

Letter from the Chair and the CEO

|

Karen Sheriff Chair, Emera Inc. Board of Directors

Scott Balfour President and Chief Executive Officer, Emera Inc. |  |  | ||

| Fellow Shareholders, | It’s a transformative era for the energy sector as economic, social, political, technological and environmental trends are shaping a future where energy is a cornerstone of progress. This is being amplified by advancements made toward the energy transition — where we’re experiencing a fundamental shift in how energy is generated, delivered and consumed. | |||

| Our sector saw numerous challenges, and opportunities throughout the year including evolving customer expectations, customer affordability challenges, unprecedented weather events, supply chain constraints, evolving government and energy policy and ongoing global economic and geopolitical impacts. | ||||

| Our operating companies rose to these challenges and seized opportunities, staying focused on reliably and cost effectively delivering for customers today, while working to ensure we can continue to meet their needs in the future. This commitment to customers and operational excellence enables Emera to stay focused on providing sustainable, long- term value to shareholders. | ||||

| Our operating teams’ commitment to customers was exemplified in 2024 by the response to two record-breaking storms that impacted our Florida utilities. Hurricane Helene hit in late September, followed less than two weeks later by Hurricane Milton — the strongest storm to hit Tampa Bay in a century. After Milton, more than 6,000 workers, including teams from Nova Scotia Power and across the continent, worked nonstop to restore service to hundreds of thousands of Tampa Electric customers within a week, logging over 900,000 work hours in tough conditions with no serious safety incidents. | ||||

| In recognition of this outstanding work, the Tampa Electric team was awarded the Edison Electric Institute Emergency Response Award for 2024. We’re incredibly proud of our team’s dedication to customers despite the challenging circumstances. | ||||

| The Peoples Gas system fared very well, with fewer than 1,500 of its more than 500,000 customers experiencing service interruptions during the hurricanes. As electric utilities focused on safely restoring power, Peoples Gas provided critical emergency backup energy for homes, businesses, shelters and healthcare facilities, demonstrating the resilience and | ||||

| 4 | EMERA 2024 ANNUAL REPORT |

reliability of natural gas and its essential role in Florida’s energy system. The team also took steps to protect the system from damage during the restoration, launching a targeted damage prevention campaign to reinforce the importance of safe-digging practices in affected areas. This exceptional level of dedication to customers is shared by every member of the team across Emera — and it’s reinforced by our unwavering commitment to operational excellence and to delivering increasing value to shareholders. As a result, we accomplished a lot together, for customers and shareholders, throughout the year. 2024 Highlights We achieved a number of significant milestones in 2024 as we continued to focus our efforts on driving growth and enhancing shareholder value. We successfully executed our strategic plan to strengthen our balance sheet, create flexibility in our capital funding program and optimize our portfolio for future growth. This included the sale of our interest in the Labrador-Island Link, which closed in June, and the sale of New Mexico Gas, expected to close later this year. Once complete, these will generate combined proceeds that exceed our $1.3 billion target by more than double. We completed a $500 million issuance of hybrid securities, primarily used to repay long-term holding company debt. We moderated our dividend growth rate to provide more flexibility in financing the robust capital profile we have in front of us, while also continuing to deliver growing dividends for investors. EMERA 2024 ANNUAL REPORT 5

Letter from the Chair and the CEO

Our ambitious plan positions us well to seize growth opportunities ahead

$3.2B capital plan for 2024 completed | In Nova Scotia, we worked with the federal and provincial governments, to securitize more than $600 million of under-recovered fuel costs and deferred fuel costs at Nova Scotia Power, reducing debt and decreasing the impact from the recovery of these costs from customers through rates.

| |

| Executing on our ambitious plan supports our premium portfolio of high-quality assets across North America and positions us well to seize the growth opportunities ahead.

| ||

49% reduction in CO2 emissions since 2005 | We successfully completed our $3.2 billion capital plan for the year — our largest annual program to date — as we continued to invest in reliability and resiliency, system expansion to meet customer growth, as well as renewables and renewable integration investments largely to meet legislated decarbonization requirements in some of our jurisdictions. As a result, we made significant achievements across the Company in 2024, including:

| |

| • At the end of 2024, we achieved a 49 per cent reduction in CO2 emissions and reduced our use of coal in generation by 80 per cent, both compared to 2005 levels.1

| ||

| • Tampa Electric continued to expand its solar fleet in 2024. Two new projects totaling 100 MW were brought into service, bringing total solar capacity to 1,350 MW. Another 745 MW is planned to be added by the end of 2028. In addition to supporting reliability, solar generation has saved Tampa Electric customers $321 million USD in fuel costs since 2017. | ||

| • Peoples Gas constructed pipelines to two renewable natural gas (RNG) producers to connect additional RNG into Florida’s natural gas supply. In addition to the three RNG facilities already connected, the team is building pipelines to connect the Polk County municipal landfill and Southern Cross Dairy facilities to the intrastate transmission pipeline. The dairy connection will be bidirectional, allowing the facility to access natural gas as a reliable backup during a power outage. Both connections are expected to be in service this year. | ||

| • After receiving regulatory approval in 2024, Nova Scotia Power started construction of its 150 MW grid-scale battery storage project, an equity partnership with Nova Scotia’s 13 Mi’kmaq communities. The project includes three 50 MW battery storage sites that will enable more renewable energy and enhance reliability for customers. Two sites are expected to be operational this year, with the third to be complete in 2026. | ||

| • The Maritime Link performed well in 2024, once again achieving over 99.9 per cent availability. The Link delivered nearly two million megawatts of clean hydroelectricity to Nova Scotia, serving approximately 19 per cent of Nova Scotia Power’s energy requirements and resulting in $100M in savings for Nova Scotians over the course of the year. | ||

| 1 | Reductions are still undergoing verification. CO2 emissions reduction includes Scope 1 generation emissions for Tampa Electric and Nova Scotia Power only. |

| 6 | EMERA 2024 ANNUAL REPORT |

Letter from the Chair and the CEO Safety is our first priority in everything we do across Emera. We continue to reinforce our strong safety culture and have made significant progress in reducing serious injuries and fatalities across our operations. Grand Bahama Power has solar energy in its mix for the first time with agreements to purchase a total of 14.5 MW from three independent solar sites, two of which were commissioned in 2024. The team is also working to launch its own 5 MW solar site later this year. Once complete, solar energy at GBPC will total 19.5 MW, or approximately 14.5 per cent of the island’s energy needs. In addition to reducing CO2 emissions, solar is helping to reduce the impact of volatile fuel prices and stabilize energy costs for customers. New rates came into effect for two of our utilities in 2024 — at Peoples Gas early in January, and at New Mexico Gas in October. In December, the Florida Public Service Commission approved essentially all of Tampa Electric’s capital plan based upon a midpoint return on equity of 10.5%, with an allowed range of 9.5% to 11.5%. New rates went into effect in January 2025. In December, we announced our five-year capital investment plan — the largest in our history at $20 billion through 2029. In addition to delivering exceptional value to customers, our $20B capital plan will drive top-tier rate base growth and support our targeted annual adjusted EPS growth of five to seven per cent through 2027.1, 2 five-year capital investment plan 1 Adjusted EPS is a non-GAAP ratio, which does not have standardized meaning under USGAAP. For more information, refer to “Non-GAAP Financial Measures and Ratios” in Emera’s Q4 2024 MD&A. 2 Adjusted EPS growth forecast uses 2024 as base year. EMERA 2024 ANNUAL REPORT 7

Letter from the Chair and the CEO

Emera is well-positioned to capitalize on opportunities to deliver for our customers and our shareholders.

| Safety | ||

| Safety is a top priority in everything we do across Emera. We continue working to reinforce our strong safety culture and remain relentlessly focused on reducing serious injuries and fatalities across our operations. | ||

| Our commitment to safety is strengthened by visible safety leadership, and we continually work to build on this. Throughout 2024, members of the leadership team conducted safety engagements across the business. This included participating in a wide range of activities such as risk assessments, compliance checks, inspections and safety conversations. We believe these engagements allow leaders to underpin our commitment with frontline employees, further reinforcing our robust safety culture. | ||

| Despite remaining well under the industry average, our key safety metrics for 2024 were disappointing. We saw a 30 per cent increase in our year-over-year total recordable injury rate, placing us 24 per cent higher than our five-year average. Our lost time injury (LTI) frequency rate for the year increased by 40 per cent over 2023, three per cent higher than our five-year average. | ||

| We’re committed to learning from all incidents as we stay focused on safety first and continue working to build an Emera where no one gets hurt. | ||

|

| Financial Results | |

| $849M annual adjusted net income1 | We reported annual adjusted net income1 for 2024 of $849 million and adjusted EPS1 of $2.94. These results were in line with $2.96 in 2023 and the benchmark for our adjusted EPS growth guidance.

| |

| Our regulated utilities, particularly those in Florida, continue to drive our earnings growth with a six per cent increase in adjusted earnings1 contributions in 2024. Adjusted earnings1 growth across our regulated utilities was offset by lower earnings from equity investments as a result of the Labrador Island Link transaction in Q2 2024 and lower contributions from Emera Energy due to less favourable market conditions. | ||

| We remained focused on delivering value to our shareholders. In 2024, our Board of Directors approved an increase in our quarterly dividend of $0.03 per common share, marking our 18th consecutive year of dividend increases. This increase was in line with our adjusted dividend growth targetannounced as partofour strategic update in June. We also announced our three-year average adjusted EPS1 growth target of five to seven per cent through 2027,2 reflecting our confidence in our continued growth and strong performance. Emera shareholders can continue to expect dependable and growing dividends, underpinned by our prudent financial management and disciplined capital allocation. | ||

| 1 | Adjusted net income and adjusted EPS are a non-GAAP measure and a non-GAAP ratio, respectively, which do not have standardized meaning under USGAAP. For more information and a reconciliation to the nearest GAAP measure, refer to “Non-GAAP Financial Measures and Ratios” in Emera’s Q4 2024 MD&A. |

| 2 | Adjusted EPS growth forecast uses 2024 as base year. |

| 8 | EMERA 2024 ANNUAL REPORT |

Letter from the Chair and the CEO

| We saw a positive response to the strategic update we provided to the market mid-year. We saw strong share price performance in the second half of the year, both on an absolute and relative basis. We outperformed our closest peers on both the Canadian and US utility indices, as well as on the broader market. | ||

| With key trends converging to drive an unprecedented increase in demand for reliable energy, our growth drivers remain strong, evidenced by our forecasted seven to eight per cent rate-base growth CAGR over the next five years, as we invest to meet customer needs. We’re confident that as we make these customer-focused investments, we will also deliver long-term value for Emera shareholders. | ||

| Board Changes | ||

| After more than 10 years of service, Jackie Sheppard stepped down as Chair of the Emera Board in February 2025. Jackie’s leadership and her expertise in strategic planning, public markets, legal and corporate governance were critical in guiding Emera through a period of significant growth and expansion, including the 2016 acquisition of TECO and the successful completion of the Maritime Link project. We will continue to benefit from her expertise as she stays on as a Director through 2025. On behalf of the entire Board and management team, thank you Jackie for your invaluable commitment to Emera. | ||

| Karen Sheriff has been appointed the new Chair of the Board. Since joining as a Director in 2021, Karen’s leadership experience in public and private companies, as well as in regulated environments, has made her a strong addition to the Board and will be instrumental in guiding Emera’s next phase of growth. | ||

| We welcomed Carla Tully to the Board in June 2024. Carla is the former Chief Executive Officer and Co-Founder of Earthrise Energy. Her profound experience in the energy and infrastructure sectors in North America and Europe, combined with her track record in leading and growing businesses, have made her a strong addition to our Board. | ||

| It’s been a busy year of progress. With a stronger balance sheet, a disciplined capital investment plan, and a premium portfolio of assets located in high-quality jurisdictions across North America, Emera is well-positioned to capitalize on opportunities to deliver for our customers and our shareholders. | Thank You | |

| This a direct result of the hard work and talent of the teams across our business that drive our success. | ||

| To the Board of Directors and the entire Emera team, thank you for your relentless focus on customers and continued commitment to shareholders. Together, we’ve made great progress, and our business is well-placed for future growth. | ||

| To our valued shareholders, thank you for your confidence in Emera. | ||

|  | |||

| Karen Sheriff | Scott Balfour | |||

| Chair, Board of Directors, | President and Chief Executive Officer, | |||

| Emera Inc. | Emera Inc. |

| EMERA 2024 ANNUAL REPORT | 9 |

Financial Review

| 12 | Forward-looking Information | |

| 12 | Introduction and Strategic Overview | |

| 13 | Non-GAAP Financial Measures and Ratios | |

| 15 | Consolidated Financial Review | |

| 15 | Significant Items Affecting Earnings | |

| 16 | Consolidated Financial Highlights | |

| 18 | Consolidated Income Statement Highlights | |

| 20 | Business Overview and Outlook | |

| 20 | Florida Electric Utility | |

| 21 | Canadian Electric Utilities | |

| 23 | Gas Utilities and Infrastructure | |

| 24 | Other Electric Utilities | |

| 25 | Other | |

| 26 | Consolidated Balance Sheet Highlights | |

| 27 | Other Developments | |

| 29 | Financial Highlights | |

| 29 | Florida Electric Utility | |

| 30 | Canadian Electric Utilities | |

| 32 | Gas Utilities and Infrastructure | |

| 34 | Other Electric Utilities | |

| 36 | Other | |

| 38 | Liquidity and Capital Resources | |

| 39 | Consolidated Cash Flow Highlights | |

| 40 | Working Capital | |

| 40 | Contractual Obligations | |

| 41 | Forecasted Consolidated | |

| Capital Expenditures | ||

| 41 | Debt Management | |

| 43 | Credit Ratings | |

| 43 | Guaranteed Debt | |

| 44 | Outstanding Stock Data | |

| 45 | Pension Funding | |

| 45 | Off-Balance Sheet Arrangements | |

| 46 | Dividend Payout Ratio | |

| 46 | Transactions with Related Parties | |

| 46 | Enterprise Risk and Risk Management | |

| 54 | Risk Management including Financial Instruments | |

| 56 | Disclosure and Internal Controls | |

| 56 | Critical Accounting Estimates | |

| 60 | Changes in Accounting Policies and Practices | |

| 60 | Future Accounting Pronouncements | |

| 61 | Summary of Quarterly Results | |

| 63 | Management Report | |

| 64 | Independent Auditor’s Report | |

| 68 | Report of Independent Registered Public Accounting Firm | |

| 71 | Consolidated Financial Statements | |

| 77 | Notes to the Consolidated Financial Statements | |

| 137 | Emera Leadership and Board | |

| 138 | Shareholder Information | |

| 10 | EMERA 2024 ANNUAL REPORT |

Management’s Discussion and Analysis

Management’s Discussion & Analysis

As at February 21, 2025

Management’s Discussion & Analysis (“MD&A”) provides a review of the results of operations of Emera Incorporated and its consolidated subsidiaries and investments (collectively referred to as “Emera” or the “Company”) during the fourth quarter of, and for the full year of, 2024 relative to the same periods in 2023 and selected financial information for 2022; and its financial position as at December 31, 2024 relative to December 31, 2023. The Company’s activities are carried out through five reportable segments: Florida Electric Utility, Canadian Electric Utilities, Gas Utilities and Infrastructure, Other Electric Utilities, and Other.

This MD&A should be read in conjunction with the Emera annual audited consolidated financial statements and supporting notes as at and for the year ended December 31, 2024. Emera follows United States Generally Accepted Accounting Principles (“USGAAP” or “GAAP”). Additional information related to Emera, including the Company’s Annual Information Form, can be found on Sedar+ at www.sedarplus.ca.

The accounting policies used by Emera’s rate-regulated entities may differ from those used by Emera’s non-rate-regulated businesses with respect to the timing of recognition of certain assets, liabilities, revenues and expenses. At December 31, 2024, Emera’s rate-regulated subsidiaries and investments include:

| Rate-Regulated Subsidiary or Equity Investment | Accounting Policies Approved/Examined By | |

| Subsidiary | ||

| Tampa Electric Company (“TEC”) | Florida Public Service Commission (“FPSC”) and the Federal Energy Regulatory Commission (“FERC”) | |

| Nova Scotia Power Inc. (“NSPI”) | Nova Scotia Utility and Review Board (“UARB”) | |

| Peoples Gas System, Inc. (“PGS”) | FPSC | |

| New Mexico Gas Company, Inc. (“NMGC”) | New Mexico Public Regulation Commission (“NMPRC”) | |

| SeaCoast Gas Transmission, LLC (“SeaCoast”) | FPSC | |

| Emera Brunswick Pipeline Company Limited (“Brunswick Pipeline”) | Canadian Energy Regulator (“CER”) | |

| Barbados Light & Power Company Limited (“BLPC”) | Fair Trading Commission, Barbados (“FTC”) | |

| Grand Bahama Power Company Limited (“GBPC”) | The Grand Bahama Port Authority (“GBPA”) | |

| Equity Investments | ||

| NSP Maritime Link Inc. (“NSPML”) | UARB | |

| Maritimes & Northeast Pipeline Limited Partnership and Maritimes & Northeast Pipeline, LLC (“M&NP”) | CER and FERC | |

| St. Lucia Electricity Services Limited (“Lucelec”) | National Utility Regulatory Commission | |

All amounts are in Canadian dollars (“CAD”), except for the Florida Electric Utility, Gas Utilities and Infrastructure, and Other Electric Utilities sections of the MD&A, which are reported in United States dollars (“USD”) unless otherwise stated.

| EMERA 2024 ANNUAL REPORT | 11 |

Management’s Discussion and Analysis

Forward-looking Information

This MD&A contains “forward-looking information” (“FLI”) and statements which reflect the current view with respect to the Company’s expectations regarding future growth, results of operations, performance, the expected timing and outcome of the pending sale of NMGC, business prospects and opportunities, and may not be appropriate for other purposes within the meaning of applicable Canadian securities laws. All such information and statements are made pursuant to safe harbour provisions contained in applicable securities legislation. The words “anticipates”, “believes”, “budget”, “could”, “estimates”, “expects”, “forecast”, “intends”, “may”, “might”, “plans”, “projects”, “schedule”, “should”, “targets”, “will”, “would” and similar expressions are often intended to identify FLI, although not all FLI contains these identifying words. The FLI reflects management’s current beliefs and is based on information currently available to Emera’s management and should not be read as guarantees of future events, performance or results, and will not necessarily be accurate indications of whether, or the time at which, such events, performance or results will be achieved.

FLI is based on reasonable assumptions and is subject to risks, uncertainties and other factors that could cause actual results to differ materially from historical results or results anticipated by the FLI. Factors that could cause results or events to differ from current expectations include, without limitation: regulatory and political risk; change in law risk; operating and maintenance risks; changes in economic conditions; commodity price and availability risk; liquidity and capital markets risk; changes in credit ratings; future dividend growth, rate base growth, and adjusted earnings per common share (“EPS”) growth; timing and costs associated with certain capital investments; expected impacts on Emera of challenges in the global economy; estimated energy consumption rates; maintenance of adequate insurance coverage; changes in customer energy usage patterns; developments in technology that could reduce demand for electricity; climate change risk; weather risk, including higher frequency and severity of weather events; risk of wildfires; unanticipated maintenance and other expenditures; system operating and maintenance risk; derivative financial instruments and hedging; interest rate risk; inflation risk; counterparty risk; disruption of fuel supply; country risks; supply chain risk; environmental risks; foreign exchange (“FX”); regulatory and government decisions, including changes to environmental legislation, financial reporting and tax legislation; risks associated with pension plan performance and funding requirements; loss of service area; risk of failure of information technology (“IT”) infrastructure and cybersecurity risks; uncertainties associated with infectious diseases, pandemics and similar public health threats; market energy sales prices; labour relations; and availability of labour and management resources.

Readers are cautioned not to place undue reliance on FLI, as actual results could differ materially from the plans, expectations, estimates or intentions and statements expressed in the FLI. All FLI in this MD&A is qualified in its entirety by the above cautionary statements and, except as required by law, Emera undertakes no obligation to revise or update any FLI as a result of new information, future events or otherwise.

Introduction and Strategic Overview

Emera (TSX: EMA) is a North American provider of energy services, owning and operating a portfolio of cost-of-service, rate- regulated electric and gas utilities. Its largest operations are in Florida, with additional operations in Atlantic Canada, New Mexico, and the Caribbean. Emera is headquartered in Halifax, Nova Scotia.

Emera’s business strategy is centered on continued investment in its regulated utilities, combined with a focus on operational excellence and efficiency, to safely and reliably deliver energy to its 2.6 million customers. Effective execution of these priorities supports predictable and growing earnings, cash flow and dividends for shareholders.

Earnings opportunities in regulated utilities are a function of the magnitude of net investment in the utility (known as “rate base”), the amount of equity in the capital structure, and the targeted return on that equity (“ROE”), all as established and approved through regulation. Earnings are also affected by sales volumes and operating expenses. In 2024, Emera’s regulated cost-of-service utilities in Florida accounted for 65 per cent of average consolidated rate base, with Atlantic Canada comprising 27 per cent, and the Caribbean and New Mexico at 4 per cent each.

Emera’s capital investment plan is forecasted to be approximately $20 billion from 2025 through 2029 and is focused on delivering value for customers through prudent investments in reliability and system resiliency, infrastructure modernization, expansion to address customer growth, integration of renewables, and technological innovations to deliver better customer experiences. It is anticipated that approximately 80 per cent of this capital investment will be made in Emera’s Florida utilities, necessitated by customer growth and system requirements at both TEC and PGS.

| 12 | EMERA 2024 ANNUAL REPORT |

Management’s Discussion and Analysis

| As at millions of dollars | 2025 | 2026 | 2027 | 2028 | 2029 | Total | ||||||||||||||||||

| Capital investment plan | $ | 3,420 | $ | 3,990 | $ | 4,050 | $ | 4,380 | $ | 4,590 | $ | 20,430 | ||||||||||||

| Average consolidated rate base | ||||||||||||||||||||||||

| US operations | $ | 21,520 | $ | 23,340 | $ | 25,140 | $ | 27,050 | $ | 29,400 | ||||||||||||||

| Canadian operations | 7,630 | 8,000 | 8,370 | 8,590 | 8,870 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

| Total | $ | 29,150 | $ | 31,340 | $ | 33,510 | $ | 35,640 | $ | 38,270 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

| * | Capital investment plan and average consolidated rate base exclude NMGC. Refer to “Other Developments” for more information on the pending sale of NMGC. |

Emera’s capital investment plan will be funded primarily through internally generated cash flows, debt raised at the operating company level consistent with regulated capital structures, equity issuances, and the anticipated sale of NMGC. Generally, Emera’s equity requirements are expected to be funded through the issuance of preferred equity, and the issuance of common equity through Emera’s dividend reinvestment plan (“DRIP”) and its at-the-market program (“ATM program”). Maintaining investment-grade credit ratings is a core strategic priority of the Company.

Emera has increased dividends per common share paid for 18 consecutive years and has provided forward annual dividend growth guidance of one to two per cent. Emera’s anticipates adjusted EPS average growth of five to seven per cent through 2027 which will support reduction in the ratio of dividend payout to adjusted net income. For further information on the non- GAAP ratios “Adjusted EPS” and “Dividend Payout Ratio of Adjusted Net Income”, refer to the “Non-GAAP Financial Measures and Ratios” section.

Non-GAAP Financial Measures and Ratios

Emera uses financial measures and ratios that do not have standardized meaning under USGAAP and are calculated by adjusting certain GAAP measures for specific items. They may not be comparable to similar measures presented by other entities. These measures and ratios are discussed and reconciled below.

ADJUSTED NET INCOME, ADJUSTED EPS – BASIC, AND DIVIDEND PAYOUT RATIO OF ADJUSTED NET INCOME

Emera calculates an adjusted net income attributable to common shareholders (“adjusted net income”) measure by excluding items below from net income attributable to common shareholders. Management believes excluding these items better distinguishes ongoing operations of the business and allows investors to better understand and evaluate the business.

Emera calculates adjusted net income for the Florida Electric Utility, Canadian Electric Utilities, Gas Utilities and Infrastructure, Other Electric Utilities, and Other segments. Reconciliation to the nearest GAAP measure is included in each segment. For more information refer to the Financial Highlights section for each of Florida Electric Utility, Gas Utilities and Infrastructure, Other Electric Utilities, and Other.

Adjusted EPS – basic and dividend payout ratio of adjusted net income are non-GAAP ratios which are calculated using adjusted net income, as described above. For further details on dividend payout ratio of adjusted net income, refer to the “Dividend Payout Ratio” section.

ADJUSTING ITEM IMPACTING ALL PERIODS:

Mark-to-market (“MTM”) Adjustments:

Management believes excluding from net income the effect of MTM valuations and changes thereto, until settlement, better aligns the intent and financial effect of these contracts with the underlying cash flows, and therefore excludes MTM adjustments for evaluation of performance and incentive compensation. The MTM adjustments are related to the following:

| • | held-for-trading (“HFT”) commodity derivative instruments, including adjustments related to the price differential between the point where natural gas is sourced and where it is delivered, and the related amortization of transportation capacity recognized as a result of certain Emera Energy marketing and trading transactions; |

| • | the business activities of Bear Swamp Power Company LLC (“Bear Swamp”) included in Emera’s equity income; |

| • | equity securities held in BLPC and Emera Energy; and FX hedges entered into to hedge USD denominated operating unit earnings exposure. |

| EMERA 2024 ANNUAL REPORT | 13 |

Management’s Discussion and Analysis

ADJUSTING ITEMS IMPACTING 2024:

Gain on Sale of Emera’s Indirect Minority Interest in the LIL (“Gain on sale of LIL”):

In Q2 2024, Emera recognized a $107 million gain, after tax and transaction costs, on the sale of LIL. In Q4 2024, Emera recognized a $22 million tax benefit related to the reversal of a prior year valuation allowance. A portion of the taxable capital gain on sale of LIL was offset by prior year loss carryforwards, of which the tax benefit was subject to a valuation allowance as at December 31, 2023. For further details refer to the “Significant Items Affecting Earnings” and “Other Developments” sections.

Financing Structure Wind-Up:

In Q4 2024, Emera recognized a $58 million tax benefit related to denied interest and financing expenses and the wind- up of a specific financing structure. For further details refer to the “Significant Items Affecting Earnings” and “Other Developments” sections.

Charges Related to Wind-Down Costs and Certain Asset Impairments:

In Q4 2024, the Company recognized $26 million, after-tax, in wind-down costs and certain asset impairments, primarily at Block Energy LLC (“Block Energy”). For further details, refer to the “Significant Items Affecting Earnings” section.

Charges Related to the Pending Sale of NMGC:

On August 5, 2024, Emera entered into an agreement to sell NMGC. In Q3 2024, the Company recognized $206 million in non-cash goodwill and other impairment charges, after-tax, and an additional loss of $19 million in estimated transaction costs, after-tax, related to the pending sale. For further details, refer to the “Significant Items Affecting Earnings” and “Other Developments” sections.

ADJUSTING ITEMS IMPACTING 2022:

GBPC Impairment Charge:

In Q4 2022, the Company recognized a $73 million non-cash goodwill impairment charge related to GBPC due to a decline in the fair value (“FV”) of the reporting unit.

NSPML Unrecoverable Costs:

In Q1 2022, the UARB issued a decision to disallow recovery of $9 million in costs ($7 million after-tax) included in NSPML’s final capital cost application.

RECONCILIATION OF NET INCOME ATTRIBUTABLE TO COMMON SHAREHOLDERS TO ADJUSTED NET INCOME:

| For the | Three months ended December 31 | Year ended December 31 | ||||||||||||||||||

| millions of dollars (except per share amounts) | 2024 | 2023 | 2024 | 2023 | 2022 | |||||||||||||||

| Net income attributable to common shareholders | $ | 154 | $ | 289 | $ | 494 | $ | 978 | $ | 945 | ||||||||||

| Gain on sale of LIL, after-tax (1) | 22 | — | 129 | — | — | |||||||||||||||

| Financing structure wind-up | 58 | — | 58 | — | — | |||||||||||||||

| Charges related to wind-down costs and certain asset impairments, after-tax (2) | (26 | ) | — | (26 | ) | — | — | |||||||||||||

| Charges related to the pending sale of NMGC, after-tax (3)(4) | — | — | (225 | ) | — | — | ||||||||||||||

| MTM (loss) gain, after-tax (5) | (146 | ) | 114 | (291 | ) | 169 | 175 | |||||||||||||

| GBPC impairment charge | — | — | — | — | (73 | ) | ||||||||||||||

| NSPML unrecoverable costs | — | — | — | — | (7 | ) | ||||||||||||||

| Adjusted net income | $ | 246 | $ | 175 | $ | 849 | $ | 809 | $ | 850 | ||||||||||

| EPS – basic | $ | 0.52 | $ | 1.04 | $ | 1.71 | $ | 3.57 | $ | 3.56 | ||||||||||

| Adjusted EPS – basic | $ | 0.84 | $ | 0.63 | $ | 2.94 | $ | 2.96 | $ | 3.20 | ||||||||||

| (1) | Includes an income tax recovery of $22 million for the three months ended December 31, 2024 and net of income tax expense of $53 million for the year ended December 31, 2024 (2023 – nil). |

| (2) | Net of income tax recovery of $6 million for the three months and year ended December 31, 2024 (2023 – nil). |

| (3) | Represents (i) $206 million in non-cash goodwill and other impairment charges, after-tax and (ii) $19 million in transaction costs, after-tax for the year ended December 31, 2024 (2023 – nil). |

| (4) | Net of income tax recovery of $21 million for the year ended December 31, 2024 (2023 – nil). |

| (5) | Net of income tax recovery of $57 million for the three months ended December 31, 2024 (2023 – $44 million expense) and $117 million recovery for the year ended December 31, 2024 (2023 – $68 million expense) (2022 – $73 million expense). |

| 14 | EMERA 2024 ANNUAL REPORT |

Management’s Discussion and Analysis

EBITDA AND ADJUSTED EBITDA

Earnings before interest, income taxes, depreciation and amortization (“EBITDA”) and adjusted EBITDA are non-GAAP financial measures used by Emera. These financial measures are used by numerous investors and lenders to better understand cash flows and credit quality. EBITDA is useful to assess Emera’s operating performance and indicates the Company’s ability to service or incur debt, invest in capital, and finance working capital requirements.

Adjusted EBITDA represents EBITDA excluding the income effect of the gain on sale of LIL, charges related to wind-down costs and certain asset impairments, charges related to the pending sale of NMGC, MTM adjustments, the 2022 GBPC impairment charge, and the 2022 NSPML unrecoverable costs.

RECONCILIATION OF NET INCOME TO EBITDA AND ADJUSTED EBITDA:

| For the | Three months ended December 31 | Year ended December 31 | ||||||||||||||||||

| millions of dollars | 2024 | 2023 | 2024 | 2023 | 2022 | |||||||||||||||

| Net income (1) | $ | 173 | $ | 307 | $ | 568 | $ | 1,045 | $ | 1,009 | ||||||||||

| Interest expense, net | 248 | 241 | 973 | 925 | 709 | |||||||||||||||

| Income tax (recovery) expense | (199 | ) | 51 | (159 | ) | 128 | 185 | |||||||||||||

| Depreciation and amortization | 296 | 264 | 1,162 | 1,049 | 952 | |||||||||||||||

| EBITDA | $ | 518 | $ | 863 | $ | 2,544 | $ | 3,147 | $ | 2,855 | ||||||||||

| Gain on sale of LIL, excluding income tax | — | — | 182 | — | — | |||||||||||||||

| Charges related to wind-down costs and certain asset impairments, excluding income tax | (32 | ) | — | (32 | ) | — | — | |||||||||||||

| Charges related to the pending sale of NMGC, excluding income tax | — | — | (246 | ) | — | — | ||||||||||||||

| MTM (loss) gain, excluding income tax | (203 | ) | 158 | (408 | ) | 237 | 248 | |||||||||||||

| GBPC impairment charge | — | — | — | — | (73 | ) | ||||||||||||||

| NSPML unrecoverable costs | — | — | — | — | (7 | ) | ||||||||||||||

| Adjusted EBITDA | $ | 753 | $ | 705 | $ | 3,048 | $ | 2,910 | $ | 2,687 | ||||||||||

| (1) | Net income is before Non-controlling interest in subsidiaries and Preferred stock dividends. |

Consolidated Financial Review

Significant Items Affecting Earnings

The items detailed below have had a significant impact on Net Income Attributable to Common Shareholders but have been excluded from Adjusted Net Income as described in the section entitled “Non-GAAP Financial Measures and Ratios”.

FINANCING STRUCTURE WIND-UP

During 2024, the Company incurred $185 million of interest and financing expenses in connection with a specific financing structure. The current and future interest and financing expenses are expected to be denied under the recently enacted Excessive Interest and Financing Expenses Limitation (“EIFEL”) legislation and, as a result, the financing structure has been wound up. It was determined that Emera is more likely than not to realize the benefit of the current denied interest and financing expenses in future periods and therefore a $54 million deferred income tax asset and related income tax benefit ($0.19 per common share) was recorded during Q4 2024. In addition, Emera recognized a $4 million income tax benefit ($0.01 per common share) related to the reversal of a deferred income tax liability on the wind-up of the financing structure. The total tax benefit of $58 million was recorded in “Income Tax (Recovery) Expense” on the Consolidated Statements of Income and included in the Other segment. For further details on the EIFEL legislation, refer to the “Other Developments” section.

CHARGES RELATED TO WIND-DOWN COSTS AND CERTAIN ASSET IMPAIRMENTS

In Q4 2024, Emera recognized $32 million ($26 million after-tax, or $0.09 per common share) in wind-down costs and certain asset impairments, primarily at Block Energy. These were recorded in “Other Income, net” and “Impairment Charges” on the Consolidated Statements of Income and included mainly in the Other segment.

| EMERA 2024 ANNUAL REPORT | 15 |

Management’s Discussion and Analysis

GAIN ON SALE OF LIL

On June 4, 2024, Emera completed the sale of its LIL equity interest. A gain on sale of $182 million after transaction costs ($107 million, after tax and transaction costs, or $0.37 per common share), was recognized in “Other Income, net” on the Consolidated Statements of Income in Q2 2024 and included in the Other segment. In Q4 2024, Emera recognized a $22 million ($0.08 per common share) tax benefit related to the reversal of a prior year valuation allowance. A portion of the taxable capital gain on the sale of the LIL equity interest was offset by prior year loss carryforwards, of which the tax benefit had been subject to a valuation allowance as at December 31, 2023. This tax benefit was recorded in “Income Tax (Recovery) Expense” on the Consolidated Statements of Income in Q4 2024 and included in the Other segment. For further details on the transaction, refer to the “Other Developments” section.

CHARGES RELATED TO THE PENDING SALE OF NMGC

In Q3 2024, Emera recognized non-cash goodwill and other impairment charges of $221 million ($206 after-tax, or $0.72 per common share) related to the NMGC reporting unit. These charges were recorded in “Impairment charges” on the Consolidated Statements of Income and included in the Other and Gas Utilities and Infrastructure segments, respectively. For further details on the pending sale of NMGC, refer to the “Other Developments” section. For further details on the non-cash goodwill impairment charge, refer to note 23 in the consolidated financial statements.

Additionally, in Q3 2024, Emera recorded a loss of $25 million ($19 million after-tax, or $0.06 per common share) in estimated transaction costs related to the pending sale of NMGC. These transaction costs were recorded in “Other Income, net” on the Consolidated Statement of Income and included in the Other segment. For further details, refer to the “Other Developments” section.

EARNINGS IMPACT OF MTM LOSS, AFTER-TAX

Quarter-to-date the 2023 MTM gain, after-tax, of $114 million decreased $260 million to a $146 million MTM loss, after-tax, for the same period in 2024. For the year ended, the 2023 MTM gain, after-tax, of $169 million decreased $460 million to a $291 million MTM loss, after-tax, for the same period in 2024. These decreases were primarily due to changes in existing positions, partially offset by lower amortization of gas transportation at Emera Energy Services (“EES”).

Consolidated Financial Highlights

| For the millions of dollars | Three months ended December 31 | Year ended December 31 | ||||||||||||||||||

| Adjusted net income | 2024 | 2023 | 2024 | 2023 | 2022 | |||||||||||||||

| Florida Electric Utility | $ | 120 | $ | 115 | $ | 644 | $ | 627 | $ | 596 | ||||||||||

| Canadian Electric Utilities | 77 | 68 | 232 | 247 | 222 | |||||||||||||||

| Gas Utilities and Infrastructure | 87 | 59 | 267 | 214 | 221 | |||||||||||||||

| Other Electric Utilities | 21 | 4 | 48 | 35 | 29 | |||||||||||||||

| Other | (59 | ) | (71 | ) | (342 | ) | (314 | ) | (218 | ) | ||||||||||

| Adjusted net income | $ | 246 | $ | 175 | $ | 849 | $ | 809 | $ | 850 | ||||||||||

| Gain on sale of LIL, after-tax | 22 | — | 129 | — | — | |||||||||||||||

| Financing structure wind-up | 58 | — | 58 | — | — | |||||||||||||||

| Charges related to wind-down costs and certain asset impairments, after-tax | (26 | ) | — | (26 | ) | — | — | |||||||||||||

| Charges related to the pending sale of NMGC, after-tax | — | — | (225 | ) | — | — | ||||||||||||||

| MTM (loss) gain, after-tax | (146 | ) | 114 | (291 | ) | 169 | 175 | |||||||||||||

| GBPC impairment charge | — | — | — | — | (73 | ) | ||||||||||||||

| NSPML unrecoverable costs | — | — | — | — | (7 | ) | ||||||||||||||

| Net income attributable to common shareholders | $ | 154 | $ | 289 | $ | 494 | $ | 978 | $ | 945 | ||||||||||

| 16 | EMERA 2024 ANNUAL REPORT |

Management’s Discussion and Analysis

The following table highlights significant changes in adjusted net income from 2023 to 2024:

| For the millions of dollars | Three months ended December 31 | Year ended December 31 | ||||||

| Adjusted net income – 2023 | $ | 175 | $ | 809 | ||||

| Operating Unit Performance | ||||||||

| Increased earnings at NSPI due to increased income tax recovery, partially offset by higher operating, maintenance and general expenses (“OM&G”) due primarily to a lower storm cost deferral | 31 | 19 | ||||||

| Increased earnings quarter-over-quarter at Other Electric Utilities primarily due to the timing of recovery of fuel costs and lower OM&G. Year-over-year increased primarily due to higher sales volumes, partially offset by higher OM&G | 17 | 13 | ||||||

| Increased earnings quarter-over-quarter at NMGC due to higher revenue from new base rates, partially offset by higher income tax expense. Decreased earnings year-over-year due to lower asset optimization revenue, partially offset by higher revenue from new base rates | 14 | (4 | ) | |||||

| Increased earnings at PGS due to higher revenue from new base rates and customer growth, partially offset by increased interest expense, depreciation, OM&G, and income tax expense | 11 | 58 | ||||||

| Increased earnings at TEC due to higher revenues from customer growth and new base rates, and the impact of a weaker CAD, partially offset by higher OM&G, and depreciation. Year-over-year increased earnings also due to lower income tax expense and lower interest expense, partially offset by unfavourable weather | 5 | 17 | ||||||

| Decreased earnings year-over-year at EES due to favourable hedging opportunities in Q1 2023 and less favourable market conditions in 2024 | (3 | ) | (16 | ) | ||||

| Decreased earnings at Bear Swamp primarily due to the recognition of investment tax credits in 2023 | (13 | ) | (20 | ) | ||||

| Decreased income from equity investments due to the sale of LIL equity interest | (16 | ) | (32 | ) | ||||

| Corporate | ||||||||

| Decreased deferred income tax asset valuation allowance due to utilization of tax loss carryforwards | 36 | 39 | ||||||

| Increased income tax recovery due to increased loss before provision for income taxes | 15 | 20 | ||||||

| Increased interest expense due to the impact of a weaker CAD on USD interest expense, increased total Corporate debt and increased interest rates | (9 | ) | (38 | ) | ||||

| Increased OM&G quarter-over-quarter primarily due to the timing difference in the valuation of long-term incentive expense and related hedges | (16 | ) | (1 | ) | ||||

| Other Variances | (1 | ) | (15 | ) | ||||

|

|

|

|

| |||||

| Adjusted net income – 2024 | $ | 246 | $ | 849 | ||||

|

|

|

|

| |||||

| For the | Year ended December 31 | |||||||||||

| millions of dollars | 2024 | 2023 | 2022 | |||||||||

| Operating cash flow before changes in working capital | $ | 2,194 | $ | 2,336 | $ | 1,147 | ||||||

| Change in working capital | 452 | (95 | ) | (234 | ) | |||||||

| Operating cash flow | $ | 2,646 | $ | 2,241 | $ | 913 | ||||||

| Investing cash flow | $ | (2,218 | ) | $ | (2,917 | ) | $ | (2,569 | ) | |||

| Financing cash flow | $ | (818 | ) | $ | 939 | $ | 1,555 | |||||

For further discussion of cash flow, refer to the “Consolidated Cash Flow Highlights” section.

| As at | December 31 | |||||||||||

| millions of dollars | 2024 | 2023 | 2022 | |||||||||

| Total assets | $ | 42,951 | $ | 39,480 | $ | 39,742 | ||||||

|

|

|

|

|

|

| |||||||

| Total long-term debt (including current portion) (1) | $ | 18,407 | $ | 18,365 | $ | 16,318 | ||||||

|

|

|

|

|

|

| |||||||

| (1) | On August 5, 2024, Emera announced an agreement to sell NMGC. As at December 31, 2024, NMGC’s assets and liabilities were classified as held for sale and are excluded from this table. For further details, refer to the “Other Developments” section and note 4 in the consolidated financial statements. |

| EMERA 2024 ANNUAL REPORT | 17 |

Management’s Discussion and Analysis

Consolidated Income Statement Highlights

| For the millions of dollars | Three months ended December 31 | Year ended December 31 | Year ended December 31 | |||||||||||||||||||||||||

| (except per share amounts) | 2024 | 2023 | Variance | 2024 | 2023 | Variance | 2022 | |||||||||||||||||||||

| Operating revenues | $ | 1,763 | $ | 1,972 | $ | (209 | ) | $ | 7,200 | $ | 7,563 | $ | (363 | ) | $ | 7,588 | ||||||||||||

| Operating expenses | 1,524 | 1,467 | (57 | ) | 6,120 | 5,769 | (351 | ) | 5,959 | |||||||||||||||||||

| Income from operations | $ | 239 | $ | 505 | $ | (266 | ) | $ | 1,080 | $ | 1,794 | $ | (714 | ) | $ | 1,629 | ||||||||||||

| Other (expense) income, net | $ | (29 | ) | $ | 51 | $ | (80 | ) | $ | 203 | $ | 158 | $ | 45 | $ | 145 | ||||||||||||

| Interest expense, net | $ | 248 | $ | 241 | $ | (7 | ) | $ | 973 | $ | 925 | $ | (48 | ) | $ | 709 | ||||||||||||

| Income tax (recovery) expense | $ | (199 | ) | $ | 51 | $ | 250 | $ | (159 | ) | $ | 128 | $ | 287 | $ | 185 | ||||||||||||

| Net income attributable to common shareholders | $ | 154 | $ | 289 | $ | (135 | ) | $ | 494 | $ | 978 | $ | (484 | ) | $ | 945 | ||||||||||||

| Adjusted net income | $ | 246 | $ | 175 | $ | 71 | $ | 849 | $ | 809 | $ | 40 | $ | 850 | ||||||||||||||

| Weighted average shares of common stock outstanding (in millions) | 294.1 | 277.7 | 16.4 | 289.1 | 273.6 | 15.5 | 265.5 | |||||||||||||||||||||

| EPS – basic | $ | 0.52 | $ | 1.04 | $ | (0.52 | ) | $ | 1.71 | $ | 3.57 | $ | (1.86 | ) | $ | 3.56 | ||||||||||||

| EPS – diluted | $ | 0.52 | $ | 1.04 | $ | (0.52 | ) | $ | 1.71 | $ | 3.57 | $ | (1.86 | ) | $ | 3.55 | ||||||||||||

| Adjusted EPS – basic | $ | 0.84 | $ | 0.63 | $ | 0.21 | $ | 2.94 | $ | 2.96 | $ | (0.02 | ) | $ | 3.20 | |||||||||||||

| Adjusted EBITDA | $ | 753 | $ | 705 | $ | 48 | $ | 3,048 | $ | 2,910 | $ | 138 | $ | 2,687 | ||||||||||||||

| Dividends per common share declared | $ | 0.7250 | $ | 0.7175 | $ | 0.0075 | $ | 2.8775 | $ | 2.7875 | $ | 0.0900 | $ | 2.6775 | ||||||||||||||

| Dividends per first preferred shares declared: | ||||||||||||||||||||||||||||

| Series A | $ | 0.5456 | $ | 0.5456 | $ | — | $ | 0.5456 | ||||||||||||||||||||

| Series B | $ | 1.6966 | $ | 1.5583 | $ | 0.1383 | $ | 0.6869 | ||||||||||||||||||||

| Series C | $ | 1.6085 | $ | 1.2873 | $ | 0.3212 | $ | 1.1802 | ||||||||||||||||||||

| Series E | $ | 1.1250 | $ | 1.1250 | $ | — | $ | 1.1250 | ||||||||||||||||||||

| Series F | $ | 1.0505 | $ | 1.0505 | $ | — | $ | 1.0505 | ||||||||||||||||||||

| Series H | $ | 1.5810 | $ | 1.3140 | $ | 0.2670 | $ | 1.2250 | ||||||||||||||||||||

| Series J | $ | 1.0625 | $ | 1.0625 | $ | — | $ | 1.0625 | ||||||||||||||||||||

| Series L | $ | 1.1500 | $ | 1.1500 | $ | — | $ | 1.1500 | ||||||||||||||||||||

OPERATING REVENUES

For Q4 2024, operating revenues decreased $209 million compared to Q4 2023 and, excluding decreased MTM gain of $291 million, increased $82 million. For the year ended December 31, 2024, operating revenues decreased $363 million compared to 2023 and, excluding decreased MTM gain of $559 million, increased $196 million. The increases were due to new rates at PGS, NSPI, TEC and NMGC; the impact of a weaker CAD; and increased customer growth at TEC and PGS. The increases were partially offset by lower fuel recovery clause and storm surcharge revenue (offset in OM&G) at TEC; and lower fuel revenue at NMGC. Year-over-year increase was also due to a change in the fuel cost recovery methodology for an industrial customer in 2023 at NSPI (offset in fuel for generation and purchased power).

OPERATING EXPENSES

For Q4 2024, operating expenses increased $57 million compared to Q4 2023, and, excluding charges related to wind-down costs and certain asset impairments of $4 million, increased $53 million. For the year ended December 31, 2024, operating expenses increased $351 million compared to 2023, and excluding the goodwill and other impairment charges primarily related to the pending sale of NMGC of $225 million, increased $126 million due to higher depreciation at TEC and PGS; the impact of a weaker CAD; higher OM&G due to timing of deferred clause recoveries at PGS and TEC; lower storm cost deferral and higher demand side management program costs at NSPI; and higher labour costs at PGS. This was partially offset by lower natural gas prices at NMGC, PGS and TEC and lower storm cost recognition at TEC (offset in revenue). Year-over-year increase was also due to a change in fuel cost recovery for an industrial customer in 2023 at NSPI (offset in revenue).

| 18 | EMERA 2024 ANNUAL REPORT |

Management’s Discussion and Analysis

OTHER INCOME, NET

For Q4 2024, other income, net decreased $80 million compared to Q4 2024 due to charges related to wind-down costs and certain asset impairments and higher FX losses.

For the year ended December 31, 2024, other income, net increased $45 million compared to the same period in 2023 due to the gain on sale of LIL, after transaction costs, partially offset by higher FX losses, charges related wind-down costs and certain asset impairments, transaction costs related to the pending sale of NMGC, and lower interest income.

INTEREST EXPENSE, NET

For Q4 2024, interest expense, net increased $7 million and for the year ended December 31,2024, increased $48 million compared to the same periods in 2023 due to the impact of a weaker CAD on USD interest expense, increased borrowings to support ongoing operations and higher interest rates.

INCOME TAX (RECOVERY) EXPENSE

For Q4 2024, income tax recovery increased $250 million compared to Q4 2023 due to decreased income before provision for income taxes, decreased deferred income tax asset valuation allowance and recognition of tax benefits associated with denied interest and financing expenses.

For the year ended December 31, 2024, income tax recovery increased $287 million compared to 2023 due to decreased income before provision for income taxes (excluding the gain on sale of LIL and charges related to the pending sale of NMGC), decreased deferred income tax asset valuation allowance and recognition of tax benefits associated with denied interest and financing expenses. This increased recovery was partially offset by the net tax impact of the gain on sale of LIL and charges related to the pending sale of NMGC.

NET INCOME AND ADJUSTED NET INCOME

For Q4 2024, net income attributable to common shareholders compared to Q4 2023, was favourably impacted by the $58 million tax benefit related to a specific financing structure and its wind-up and the $22 million valuation allowance reversal related to the gain on sale of LIL, and unfavourably impacted by the $26 million charges related to wind-down costs and certain asset impairments, and the $260 million decrease in MTM gains. Excluding these impacts, adjusted net income increased $71 million, primarily due to increased earnings at NSPI, Other Electric Utilities, NMGC, PGS, and TEC, and increased Corporate income tax recovery. This was partially offset by lower equity earnings from LIL; increased Corporate OM&G due to timing of long-term incentive expenses and related hedges; increased Corporate interest expense; and decreased earnings at Emera Energy.

For the year ended December 31, 2024, net income attributable to common shareholders, compared to the same period in 2023, was favourably impacted by the $129 million gain on sale of LIL, and the $58 million tax benefit related to a specific financing structure and its wind-up and unfavourably impacted by the $26 million in charges related to wind-down costs and certain asset impairments, $225 million in charges related to the pending sale of NMGC, and the $460 million decrease in MTM gains. Excluding these changes, adjusted net income increased $40 million. The increase was primarily due to increased earnings at PGS, NSPI, TEC, and Other Electric Utilities, and increased Corporate income tax recovery. This was partially offset by increased Corporate interest expense; lower equity earnings from LIL; and decreased earnings at Emera Energy.

EPS – BASIC AND ADJUSTED EPS – BASIC

For Q4 2024, EPS – basic was lower than in Q4 2023 due to the impact of decreased earnings, as discussed above, and an increase in weighted average shares outstanding. Adjusted EPS – basic was higher in Q4 2024, compared to Q4 2023, due to increased adjusted earnings as discussed above, partially offset by an increase in weighted average shares outstanding.

For the year ended December 31, 2024, EPS – basic was lower than in 2023 due to the impact of an increase in weighted average shares outstanding and decreased earnings, as discussed above. Adjusted EPS – basic was lower in 2024, compared to 2023, due to the impact of an increase in weighted average shares outstanding, partially offset by increased adjusted earnings, as discussed above.

EFFECT OF FOREIGN CURRENCY TRANSLATION

Emera operates in the United States (“US”), Canada and various Caribbean countries and, as such, generates revenues and incurs expenses denominated in local currencies which are translated into CAD for financial reporting. Changes in translation rates, particularly in the value of the USD against the CAD, can positively or adversely affect results.

| EMERA 2024 ANNUAL REPORT | 19 |

Management’s Discussion and Analysis

Results of foreign operations are translated at the weighted average rate of exchange, and assets and liabilities of foreign operations are translated at period end rates. The relevant CAD/USD exchange rates on net income attributable to common shareholders for 2024 and 2023 are as follows:

| Three months ended December 31 | Year ended December 31 | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Weighted average CAD/USD | $ | 1.37 | $ | 1.36 | $ | 1.36 | $ | 1.35 | ||||||||

| Period end CAD/USD exchange rate | $ | 1.44 | $ | 1.32 | $ | 1.44 | $ | 1.32 | ||||||||

The table below includes Emera’s significant segments whose contributions to adjusted net income are recorded in USD currency:

| For the | Three months ended December 31 | Year ended December 31 | ||||||||||||||

| millions of USD | 2024 | 2023 | 2024 | 2023 | ||||||||||||

| Florida Electric Utility (1) | $ | 85 | $ | 85 | $ | 470 | $ | 466 | ||||||||

| Gas Utilities and Infrastructure (2)(3) | 56 | 41 | 178 | 142 | ||||||||||||

| Other Electric Utilities | 15 | 3 | 35 | 26 | ||||||||||||

| Other segment (4)(5) | (33 | ) | (18 | ) | (131 | ) | (95 | ) | ||||||||

|

|

|

|

|

|

|

|

| |||||||||

| Total (1)(3)(5) | $ | 123 | $ | 111 | $ | 552 | $ | 539 | ||||||||

|

|

|

|

|

|

|

|

| |||||||||

| (1) | Excludes $2 million USD, after-tax, in other impairment charges for the three months and year ended December 31, 2024. |

| (2) | Includes USD net income from PGS, NMGC, SeaCoast and M&NP. |

| (3) | Excludes $6 million USD, after-tax, in other impairment charges associated with the pending sale of NMGC for the year ended December 31, 2024. |

| (4) | Includes Emera Energy’s USD adjusted net income from EES, Bear Swamp and interest expense on Emera Inc.’s USD denominated debt. |

| (5) | Excludes $84 million USD in MTM losses, after-tax, for the three months ended December 31, 2024 (2023 – $73 million USD MTM gain, after-tax) and $189 million in USD MTM losses, after-tax, for the year ended December 31, 2024 (2023 – $116 million USD MTM gain, after-tax). |

Weakening of the CAD increased adjusted net income by $2 million in Q4 2024 and $5 million for the year ended December 31, 2024, compared to the same periods in 2023. Impacts of the changes in the translation of the CAD include the impacts of Corporate FX hedges used to mitigate translation risk of USD earnings in the Other segment.

The translation impact of a weaker CAD on USD earnings was more than offset by the realized and unrealized losses on FX hedges used to mitigate translation risk of USD earnings, resulting in a $29 million decrease to net income in Q4 2024 and $35 million decrease to net income for the year ended December 31, 2024, compared to the same periods in 2023.

Business Overview and Outlook

Florida Electric Utility

The Florida Electric Utility segment consists of TEC, a vertically integrated regulated electric utility engaged in the generation, transmission and distribution of electricity, serving customers in West Central Florida. TEC has $13 billion USD of assets and approximately 855,000 customers at December 31, 2024. TEC owns 6,620 megawatts (“MW”) of generating capacity, of which 73 per cent is natural gas fired, 20 per cent is solar and 7 per cent is coal. TEC also owns 2,192 kilometres of transmission facilities and 20,693 kilometres of distribution facilities. TEC meets the planning criteria for reserve capacity established by the FPSC, which is a 20 per cent reserve margin over firm peak demand.

Beginning in 2025, TEC’s approved regulated ROE range is 9.50 per cent to 11.50 per cent (2024 – 9.25 per cent to 11.25 per cent) based on an allowed equity capital structure of 54 per cent (2024 – 54 per cent). An ROE of 10.50 per cent (2024 – 10.20 per cent) is used for the calculation of the return on investments for clauses.

TEC anticipates earning within its ROE range in 2025. As a result of new base rates effective January 1, 2025, TEC’s 2025 USD earnings are expected to be higher than in 2024. Normalizing 2024 for weather, TEC’s sales volumes in 2025 are projected to be higher than in 2024 due to customer growth. TEC expects customer growth rates in 2025 to be comparable to 2024, reflective of the expected economic growth in Florida.

| 20 | EMERA 2024 ANNUAL REPORT |

Management’s Discussion and Analysis

On April 2, 2024, TEC filed a rate case with the FPSC for new base rates. On December 3, 2024, the FPSC rendered a decision which includes annual base rate increases of $185 million USD in 2025 and adjustments of $87 million USD and $9 million USD in 2026 and 2027, respectively. The rates include recovery of solar generation projects, energy storage capacity, a more resilient and modernized energy control center, and other resiliency and reliability projects. The allowed equity in the capital structure will continue to be 54 per cent from investor sources of capital and the allowed regulatory ROE range is 9.50 per cent to 11.50 per cent with a 10.50 per cent midpoint. On February 3, 2025, the FPSC issued the final order approving the decision, effective January 1, 2025. On February 18, 2025, a motion for reconsideration on certain aspects of the rate case order was filed with the FPSC. TEC will respond to this motion in February 2025. TEC expects the FPSC to reach a final decision on the motion in Q2 2025.

On September 26, 2024, Hurricane Helene passed 100 miles west of Tampa and made landfall approximately 200 miles north of Tampa, in Taylor County, as a Category 4 hurricane. TEC’s service territory was impacted by the tropical storm force winds and storm surge which resulted in a peak number of customers out of 100,000. As of December 31, 2024, TEC deferred $49 million USD to the storm reserve for future recovery.

On October 9, 2024, Hurricane Milton made landfall approximately 50 miles south of Tampa, near Sarasota, and was the worst weather event to impact the area in over 100 years. The Category 3 hurricane had a significant impact on TEC’s service territory which resulted in a peak number of customers out of 600,000. As of December 31, 2024, TEC deferred $340 million USD to the storm reserve for future recovery.

As at December 31, 2024, total restoration costs charged to the storm reserve account have exceeded the storm reserve balance (for additional details on the storm reserve, refer to note 7 in Emera’s consolidated financial statements) and therefore $377 million USD has been deferred as a regulatory asset for future recovery. On February 4, 2025, the FPSC approved TEC’s petition filed on December 27, 2024 for the recovery of $466 million USD for costs associated with Hurricane Idalia, Hurricane Debby, Hurricane Helene and Hurricane Milton and the associated interest to replenish the storm reserve over an 18-month recovery period beginning in March 2025. The amount of cost-recovery is subject to a true-up mechanism with the FPSC.

On April 2, 2024, TEC requested a mid-course adjustment to its fuel and capacity charges, reflecting a $138 million USD reduction over 12 months, from June 2024 through May 2025. The requested reduction was due to a decrease in actual and projected 2024 natural gas prices since TEC submitted its projected 2024 costs in the fall of 2023. On May 7, 2024, the FPSC approved the mid-course adjustment.

In 2025, capital investment in the Florida Electric Utility segment is expected to be $1.7 billion USD (2024 – $1.4 billion USD), including allowance for funds used during construction (“AFUDC”). Capital projects include solar investments, grid modernization, storm hardening investments, building resilience and energy storage.

Canadian Electric Utilities

The Canadian Electric Utilities segment includes NSPI and NSPML. NSPI is a vertically integrated regulated electric utility engaged in the generation, transmission and distribution of electricity and the primary electricity supplier to customers in Nova Scotia. NSPML is a 100 per cent equity interest in the Maritime Link Project (“Maritime Link”), a transmission project between the island of Newfoundland and Nova Scotia.

On June 4, 2024, Emera completed the sale of its LIL equity interest. For further information, refer to the “Significant Items Affecting Earnings” and “Other Developments” sections.

NSPI

With $7.1 billion of assets and approximately 557,000 customers at December 31, 2024, NSPI owns 2,422 MW of generating capacity, of which 44 per cent is coal and/or oil-fired; 28 per cent is natural gas and/or oil; 19 per cent is hydro, wind, or solar; 7 per cent is petroleum coke (“petcoke”) and 2 per cent is biomass-fueled generation. In addition, NSPI has contracts to purchase renewable energy from independent power producers (“IPPs”) and community feed-in tariff (“COMFIT”) participants, which own 533 MW of capacity. NSPI also has rights to 153 MW of Maritime Link capacity, representing Newfoundland and Labrador Hydro’s (“NLH”) Nova Scotia Block (“NS Block”) delivery obligations, as discussed below. NSPI owns approximately 5,000 kilometres of transmission facilities and 28,000 kilometres of distribution facilities.

NLH is obligated to provide NSPI with approximately 900 Gigawatt hours (“GWh”) of energy annually over 35 years. In addition, for the first five years of the NS Block, NLH is obligated to provide approximately 240 GWh of additional energy from the Supplemental Energy Block transmitted through the Maritime Link. NSPI has the option of purchasing additional market-priced energy from NLH through the Energy Access Agreement. The Energy Access Agreement enables NSPI to access a market-priced bid from NLH for up to 1.8 Terawatt hours (“TWh”) of energy in any given year and, on average, 1.2 TWh of energy per year through August 31, 2041.

| EMERA 2024 ANNUAL REPORT | 21 |

Management’s Discussion and Analysis

NSPI’s approved regulated ROE range is 8.75 per cent to 9.25 per cent, based on an actual five-quarter average regulated common equity component of up to 40 per cent of approved rate base.

NSPI anticipates earning below its allowed ROE range in 2025. NSPI expects earnings in 2025 to be consistent with 2024. Sales volumes are expected to be higher in 2025 than 2024.

On September 24, 2024, the Government of Canada finalized an agreement with NSPI, NSPML and the Province of Nova Scotia (the “Province”) on terms and conditions for a federal loan guarantee (“FLG”) of $500 million in debt to be issued by NSPML to help Nova Scotia customers manage unrecovered costs of the replacement energy that was required during the several years of delay in the Muskrat Falls hydroelectricity project. On September 25, 2024, NSPI and NSPML filed applications with the UARB related to the FLG. On November 29, 2024, the UARB approved NSPML’s application to issue the debt, transfer the proceeds to NSPI as a refund of a portion of previous NSPML assessment payments (“NSPML Refund”), and to increase its annual assessment charge to NSPI to recover the refund and related financing costs over a 28-year period. On December 16, 2024, the net proceeds of the NSPML debt issuance were transferred to NSPI and applied against the FAM regulatory asset balance. On February 18, 2025, the UARB approved NSPI’s application to increase 2025 fuel rates to service the incremental NSPML debt.

On December 2, 2024, the UARB approved the recovery of $24 million of major storm restoration and incremental financing costs deferred to NSPI’s storm rider in 2023 to be recovered over a 12-month period beginning on January 1, 2025.

On June 27, 2024, the UARB approved the deferred recognition of $25 million in incremental operating costs incurred during the Hurricane Fiona storm restoration efforts in September 2022. Following UARB approval, the $25 million was reclassified to “Regulatory assets” from “Other long-term assets”. The UARB also directed NSPI to reclassify $10 million of undepreciated costs related to assets retired because of Hurricane Fiona to “Regulatory assets” from “PP&E” on the Consolidated Balance Sheets. NSPI began amortizing both of these regulatory assets over a 10-year period beginning July 1, 2024.

On June 13, 2024, the UARB approved $238 million of capital investment, including AFUDC, for the Battery Energy Storage System Project. The project is comprised of three 50 MW, four-hour battery facilities. Two facilities are anticipated to be in- service in late 2025 and the third facility in 2026.

On April 17, 2024, the UARB approved the sale of $117 million of the FAM regulatory asset to Invest Nova Scotia, a provincial Crown corporation. On April 30, 2024, the transaction closed and the $117 million was remitted to NSPI, which resulted in a corresponding decrease of the FAM regulatory asset. NSPI is collecting the amortization and financing costs related to the $117 million from customers on behalf of Invest Nova Scotia over a 10-year period, which began in Q2 2024, and is remitting those amounts to Invest Nova Scotia quarterly.

In 2025, capital investment, including AFUDC, is expected to be $480 million (2024 – $487 million). NSPI is primarily investing in capital projects required to support power system reliability and reliable service for customers.

ENVIRONMENTAL LEGISLATION AND REGULATIONS

NSPI is subject to environmental laws and regulations set by both the Government of Canada and the Province. NSPI continues to work with both levels of government to comply with these laws and regulations to maximize efficiency of emission control measures and minimize customer cost. NSPI anticipates that costs prudently incurred to achieve legislated compliance will be recoverable under NSPI’s regulatory framework. NSPI faces risks associated with achieving climate-related and environmental legislative requirements, including the risk of non-compliance, which could adversely affect NSPI’s operations and financial performance. For further discussion on these risks and environmental legislation and regulations, refer to the “Enterprise Risk and Risk Management” section. Recent developments related to provincial and federal environmental laws and regulations are outlined below.

Clean Electricity Regulations (“CER”):